What happens if I miss a car loan payment in Canada, Missing a car loan payment in Canada can be a stressful experience, especially if you’re unsure of the consequences or how to navigate the situation. What happens if I miss a car loan payment in Canada is a common concern for many Canadians facing financial challenges. Whether it’s a one-time oversight or part of ongoing financial difficulties, understanding the implications, processes, and solutions can help you make informed decisions.

What happens if I miss a car loan payment in Canada, This article explores the effects of missing a car loan payment, offers actionable steps, and provides insights from authoritative sources like government and bank websites. For personalized assistance, resources like Quick Approvals can guide you through managing your car loan effectively.

Consequences of Missing Car Loan Payment in Canada

What happens if I miss a car loan payment in Canada, When you miss a car loan payment, several immediate and long-term consequences may arise, depending on your lender’s policies and the terms of your loan agreement. Typically, lenders in Canada impose penalties for late payments, which can include late fees ranging from $25 to $100, depending on the contract. These fees add to your financial burden, making it harder to catch up.

Beyond fees, missing a payment can lead to increased interest charges, as some lenders may apply a higher default interest rate to overdue balances. According to the Government of Canada’s Financial Consumer Agency, lenders must disclose such penalties in the loan agreement, so reviewing your contract is critical.

- Late Fees: Most lenders charge a flat fee or a percentage of the overdue amount.

- Interest Rate Hikes: Some agreements allow lenders to increase interest rates on overdue balances.

- Communication from Lender: Expect calls or letters from your lender reminding you of the missed payment.

If the missed payment remains unresolved, it can escalate to more severe consequences, such as damage to your credit score or even vehicle repossession, which we’ll explore in later sections.

Effects of Missing a Car Loan Payment in Canada

Missing a car loan payment can have ripple effects on your financial health. One of the most immediate impacts is on your credit report. In Canada, payment history accounts for 35% of your credit score, according to Equifax Canada. A single missed payment, if reported, can lower your score by 50-100 points, depending on your credit history. This can affect your ability to secure future loans or credit cards.

Additionally, lenders may report the delinquency to credit bureaus like Equifax or TransUnion after 30 days, marking it as a “late payment.” Multiple missed payments can lead to a “default” status, further damaging your credit. For detailed insights on credit reporting, the Government of Canada’s credit report guide provides a comprehensive overview.

Other effects include:

- Reduced Borrowing Power: A lower credit score may lead to higher interest rates on future loans.

- Collection Actions: After 60-90 days, lenders may involve collection agencies, increasing stress and financial pressure.

- Emotional Stress: Constant communication from lenders can add to financial anxiety.

How Missing Car Loan Affects Credit Score Canada

How missing car loan affects credit score Canada is a critical question for borrowers. As mentioned, payment history is a significant factor in your credit score. A missed payment reported to credit bureaus can remain on your credit report for up to six years in Canada, impacting your financial opportunities. The severity depends on how late the payment is (e.g., 30, 60, or 90 days) and how frequently you miss payments.

For example, a single 30-day late payment may cause a temporary dip, but consistent missed payments can lead to a “serious delinquency” status, significantly lowering your score. Data from competitor websites like Ratehub.ca suggests that maintaining open communication with your lender can sometimes prevent reporting to credit bureaus, especially if you resolve the payment quickly.

To mitigate credit damage: How missing car loan affects credit score Canada

- Pay the overdue amount as soon as possible.

- Contact your lender to negotiate a payment plan.

- Monitor your credit report regularly to ensure accuracy.

What to Do After Missing Car Payment Canada

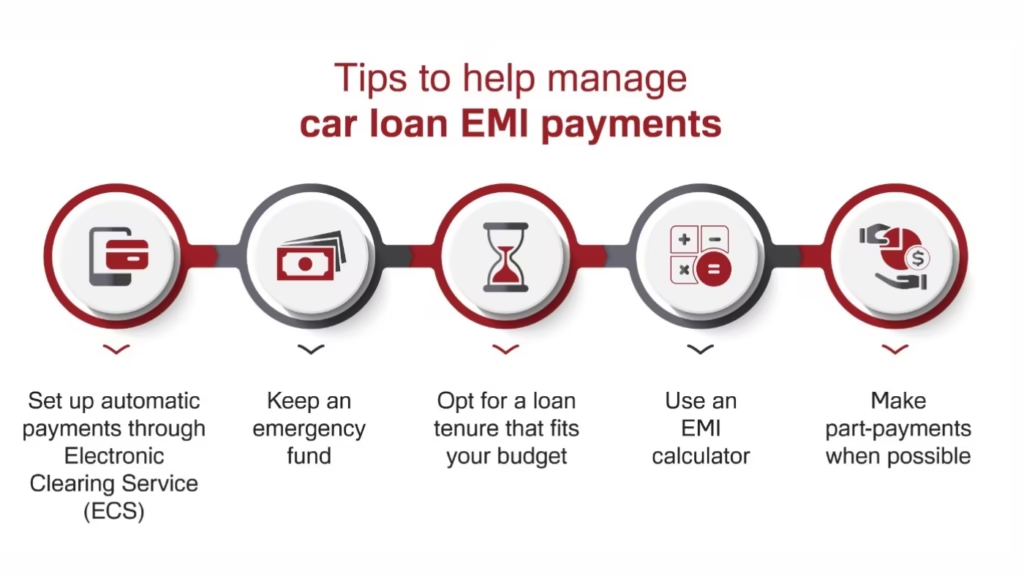

If you’ve missed a payment, acting quickly is essential to minimize the fallout. What to do after missing car payment Canada involves proactive steps to address the issue and prevent further consequences. First, review your loan agreement to understand the lender’s policies on late payments, grace periods, and penalties. Most Canadian lenders offer a grace period of 7-15 days before reporting to credit bureaus.

Next, contact your lender immediately to explain your situation. Many lenders, including major banks like RBC or TD, are willing to work with borrowers facing temporary financial difficulties. Options may include:

- Payment Deferral: Temporarily pausing payments, though interest may still accrue.

- Modified Payment Plan: Adjusting monthly payments to a more manageable amount.

- Lump-Sum Catch-Up: Paying the missed amount plus fees to bring the loan current.

What to do after missing car payment Canada, For tailored solutions, Quick Approvals offers resources to help you navigate car loan challenges and connect with lenders who understand your needs.

Penalties for Late Car Loan Payment in Canada

Penalties for late car loan payment in Canada vary by lender but typically include monetary fines and potential credit impacts. Late fees are the most common penalty, often outlined in the loan agreement. For instance, information from competitor sites like CarLoansCanada.com indicates that fees can range from $50 to $100 per missed payment, depending on the lender’s terms.

Other penalties may include: Penalties for late car loan payment in Canada

- Default Interest Rates: Higher interest applied to overdue amounts.

- Legal Action: In extreme cases, lenders may pursue legal remedies after multiple missed payments.

- Repossession Risk: If payments remain unpaid, the lender may initiate repossession proceedings.

To avoid these penalties, prioritize communication with your lender and explore options like payment deferrals or refinancing.

Can You Defer Car Loan Payment in Canada

Can you defer car loan payment in Canada is a common question for those facing financial hardship. Many Canadian lenders offer deferral programs, allowing borrowers to pause payments for 1-3 months under certain conditions. However, deferrals are not automatic and typically require approval based on your financial situation and payment history.

Can you defer car loan payment in Canada, During a deferral, interest may continue to accrue, increasing the total loan cost. Major banks like Scotiabank often outline deferral options in their loan agreements, and contacting your lender directly is the best way to explore this option. Deferrals can provide temporary relief but should be used cautiously to avoid long-term financial strain.

Car Repossession Process After Missed Payment Canada

The car repossession process after missed payment Canada is a serious consequence that typically occurs after multiple missed payments, often 90-120 days of delinquency. In Canada, lenders must follow legal protocols outlined in provincial laws, such as Ontario’s Consumer Protection Act. The process generally includes:

- Default Notice: Lenders send a notice of default, giving you a chance to catch up on payments.

- Repossession Attempt: If payments remain unpaid, the lender may hire a repossession agency to seize the vehicle.

- Sale of Vehicle: The repossessed car is sold, and proceeds are applied to the loan balance. You may still owe any remaining debt.

Data from competitor websites like AutoLoanSolutions.ca notes that repossession can occur without court involvement in some provinces, but lenders must provide notice. To avoid repossession, act quickly to negotiate with your lender or seek professional advice.

How to Avoid Repossession After Missing Car Payment Canada

How to avoid repossession after missing car payment Canada involves proactive measures to regain control of your loan. Here are practical steps:

- Contact Your Lender: Discuss payment plans or deferrals to prevent escalation.

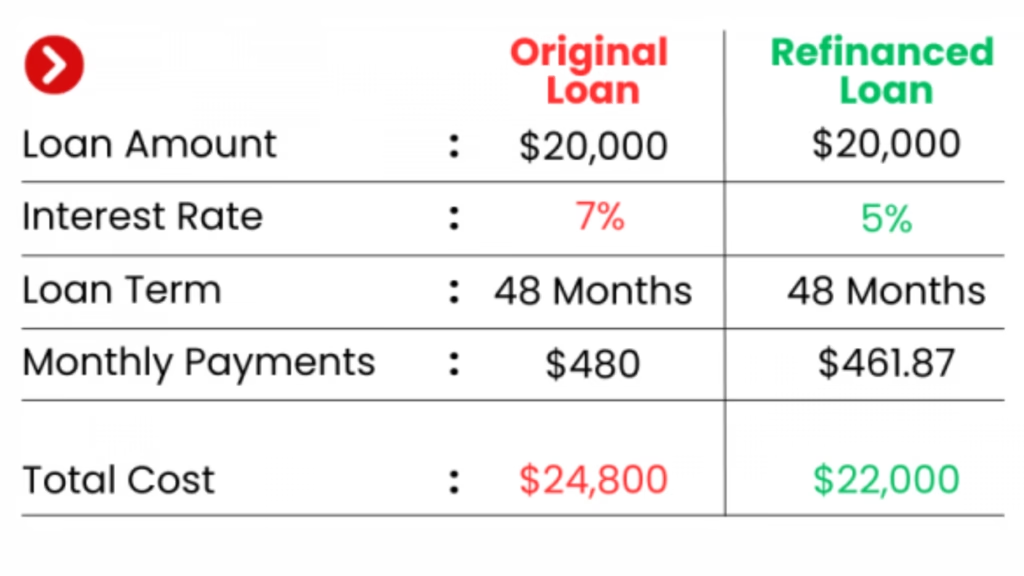

- Refinance the Loan: Lower monthly payments by extending the loan term or securing a better rate.

- Sell the Car: If payments are unsustainable, selling the car privately may cover the loan balance.

- Seek Financial Counseling: Non-profits like Credit Counselling Canada can offer guidance.

Resources like Quick Approvals can connect you with lenders offering flexible terms to help avoid repossession.

Is It Bad to Miss One Car Payment Canada

Is it bad to miss one car payment Canada depends on how quickly you address the issue. A single missed payment within the grace period (typically 7-15 days) may result in a late fee but not necessarily a credit report. However, if reported, even one missed payment can lower your credit score and signal financial instability to future lenders.

Taking immediate action, such as paying the overdue amount or negotiating with your lender, can mitigate the damage. Consistent communication is key to avoiding long-term consequences.

Q&A: Common Questions About Missing Car Loan Payments in Canada

What Happens If I Miss a Car Loan Payment in Canada?

Missing a car loan payment triggers late fees, potential interest rate increases, and credit score damage if reported after 30 days. Lenders may contact you to resolve the issue, and prolonged delinquency can lead to repossession. For more details, the Government of Canada’s car loan guide explains lender obligations.

How Missing Car Loan Affects Credit Score Canada?

A missed payment can lower your credit score by 50-100 points, depending on your credit history. Reported delinquencies stay on your credit report for six years, impacting future borrowing. Regular monitoring and timely payments can help mitigate damage.

What to Do After Missing Car Payment Canada?

Contact your lender immediately to discuss options like payment plans or deferrals. Pay the overdue amount as soon as possible to avoid credit reporting. Resources like Quick Approvals can assist in finding solutions tailored to your situation.

Can You Defer Car Loan Payment in Canada?

Yes, many lenders allow deferrals for 1-3 months, but interest may accrue. Approval depends on your financial situation and lender policies. Contact your lender directly to explore this option and understand the terms.

How to Avoid Repossession After Missing Car Payment Canada?

Prevent repossession by negotiating with your lender, refinancing, or selling the car to cover the loan balance. Financial counseling can also help. Acting quickly is crucial to avoid legal action or vehicle seizure.

Conclusion

Missing a car loan payment in Canada can lead to significant financial challenges, from late fees and credit score damage to the risk of repossession. Understanding What happens if I miss a car loan payment in Canada empowers you to take proactive steps, such as contacting your lender, exploring deferrals, or refinancing. By addressing missed payments promptly, you can minimize penalties and protect your financial health. For authoritative guidance, explore resources like the Government of Canada’s financial consumer agency, and for personalized loan solutions, visit Quick Approvals. Taking action today can help you avoid long-term consequences and maintain control over your car loan.