RV hybrid loan alternatives, Many Canadian homeowners aged 55 and older find themselves with significant equity tied up in their properties but facing cash flow challenges in retirement.

RV hybrid loan alternatives refer to flexible financial products that blend features of traditional reverse mortgages (often called “RV” in shorthand) with other home equity access options, allowing seniors to unlock tax-free funds without mandatory monthly payments or the need to sell their home. These alternatives provide a way to supplement retirement income, cover healthcare costs, or fund lifestyle needs while aging in place.

As housing values have risen across Canada, home equity has become a key asset for retirees. According to resources from the Financial Consumer Agency of Canada, borrowing against home equity offers various pathways, including lines of credit and specialized loans tailored for seniors. This article delves into the most viable RV hybrid loan alternatives, comparing their features, benefits, and considerations to help you make an informed decision.

Understanding Alternatives to Reverse Mortgage in Canada

Traditional reverse mortgages, such as the CHIP program, allow homeowners to borrow up to 55% of their home’s value with no payments required until the home is sold. However, higher interest rates and compounding can reduce remaining equity over time. RV hybrid loan alternatives

Alternatives to reverse mortgage in Canada often combine elements like flexible drawdowns, lower rates, or optional payments to create hybrid solutions better suited to individual needs.

These options are particularly relevant in 2025, with fluctuating interest rates and an aging population seeking sustainable retirement funding. Government sources emphasize that equity release products should align with long-term financial security, noting that no single option fits all scenarios.

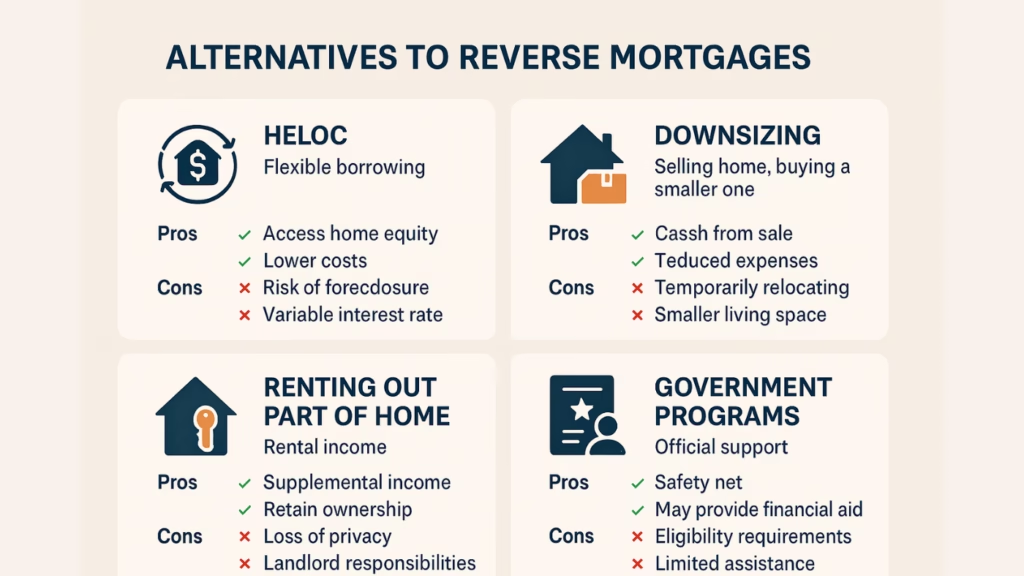

- Home Equity Lines of Credit (HELOCs) as revolving credit

- Cash-out refinancing for lump sums

- Blended products offering no-payment flexibility with rate advantages

- Downsizing as a non-borrowing alternative

Exploring these can preserve more equity for heirs while providing immediate access to funds.

The Role of HELOC as Alternative to Reverse Mortgage Canada

A standout among RV hybrid loan alternatives is the Home Equity Line of Credit (HELOC). Unlike a standard reverse mortgage, a HELOC functions like a credit card secured by your home, allowing borrowing up to 65% of the property value (or combined with a mortgage up to 80%). HELOC as Alternative to Reverse Mortgage Canada

Key advantages include lower interest rates—often variable and tied to prime—compared to reverse mortgages. You only pay interest on what you draw, and as you repay, credit becomes available again. This revolving nature makes it a hybrid option: flexible access without the full compounding burden of no-payment loans.

For seniors with some income, a HELOC can mimic reverse mortgage benefits by making interest-only payments, keeping the balance stable. Data from bank websites shows HELOCs from major institutions like RBC’s Homeline Plan or Scotiabank’s STEP offer readvanceable features, automatically increasing limits as mortgage principal decreases.

| Feature | HELOC | Traditional Reverse Mortgage |

|---|---|---|

| Borrowing Limit | Up to 65-80% combined | Up to 55% |

| Payments Required | Interest-only possible | None until due |

| Interest Rates (2025 est.) | Lower (prime + margin) | Higher (6-10%) |

| Qualification | Income/credit check | Age/home value focus |

HELOCs serve as an effective hybrid for those who qualify, blending accessibility with cost savings.

Comparing Home Equity Loan vs Reverse Mortgage Canada

Home Equity Loan vs Reverse Mortgage Canada, Fixed home equity loans provide a lump sum at closing, with required principal and interest payments over a set term. This differs from reverse mortgages’ deferred repayment but offers predictability.

In a hybrid context, some lenders allow “no-payment” home equity loans for seniors, where interest accrues similarly to a reverse mortgage but with potentially lower rates or fees. Refinancing to cash out equity is another variant: replace your existing mortgage with a larger one, pocketing the difference.

- Pros: Lower rates than reverse; fixed payments build discipline

- Cons: Monthly obligations strain fixed incomes

- Hybrid appeal: Combine with interest-only options for flexibility

For many, this comparison highlights why hybrids—blending lump-sum access with optional payments—are gaining traction in Canada. Home Equity Loan vs Reverse Mortgage Canada

Exploring Hybrid Home Equity Loan Options Canada

True hybrids merge reverse mortgage no-payment features with HELOC flexibility or lower-cost structures. Products like readvanceable mortgages (e.g., Manulife One or bank “all-in-one” accounts) bundle a mortgage with a HELOC, allowing automatic reborrowing as principal pays down.

In 2025, some alternative lenders offer equity-based products without strict income proofs, closer to reverse mortgages but with capped compounding. These hybrid home equity loan options Canada appeal to retirees wanting to minimize interest growth while accessing funds on-demand.

Benefits include:

- Tax-free cash draws

- Optional prepayments to control balance

- Potential for lower setup fees

Consulting resources like Canada.ca’s guide on borrowing against home equity can clarify these blended products.

No Payment Home Equity Loan Canada: A Core Hybrid Feature

The hallmark of many RV hybrid loan alternatives is the no-payment structure. Similar to reverse mortgages, interest accrues and adds to the balance, repaid upon sale. This eliminates monthly strain, ideal for fixed-income seniors.

However, hybrids often cap accrual or allow voluntary interest payments to preserve equity. In Canada, such options are available through specialized lenders, providing up to 55% equity access without mandatory repayments.

This feature supports aging in place, with funds for renovations, healthcare, or travel.

Downsizing vs Reverse Mortgage Canada: Non-Borrowing Alternative

Not all alternatives involve loans. Downsizing—selling your larger home and buying smaller—releases equity outright, often mortgage-free.

Pros:

- No debt or interest

- Lower ongoing costs (taxes, maintenance)

- Lump-sum cash for investments

Cons:

- Emotional/uprooting costs

- Transaction fees (5-6% typical)

- Potential land transfer taxes

Compared to hybrids, downsizing maximizes inheritance but requires moving. Many prefer hybrid loans to stay put.

Other Equity Release Options Without Reverse Mortgage Canada

Beyond HELOCs and loans, options include selling and renting back, or family equity-sharing agreements. Government resources note personal loans or credit lines as unsecured alternatives, though higher rates apply.

For seniors, Canadian seniors home equity alternatives increasingly include blended bank products combining fixed mortgages with revolving credit.

Q&A: Common Questions on RV Hybrid Loan Alternatives

What are alternatives to reverse mortgage in Canada?

Alternatives include HELOCs, home equity loans, refinancing, and downsizing. Hybrids blend no-payment access with flexible terms, often at lower costs. See FCAC’s reverse mortgage overview for comparisons.

How does a HELOC as alternative to reverse mortgage Canada work?

A HELOC provides revolving credit up to 65% equity, with interest-only payments possible. It’s ideal if you have income to cover interest, avoiding compounding like in pure reverse mortgages.

What are the best reverse mortgage alternatives Canada for no payments?

No payment home equity loan Canada options mimic reverse mortgages but may offer better rates or prepayment flexibility. Hybrids from banks provide similar benefits.

Is downsizing vs reverse mortgage Canada better for inheritance?

Downsizing often preserves more equity for heirs by avoiding interest accrual, but hybrids allow voluntary payments to control growth.

How to access home equity without reverse mortgage Canada?

Use a HELOC, refinance, or fixed equity loan. These require payments but typically have lower rates, blending well for hybrid needs.

What are hybrid home equity loan options Canada in 2025?

Blended products like readvanceable accounts or senior-focused equity lines combine fixed and revolving access, with optional no-payment periods.

Conclusion: Choosing the Right RV Hybrid Loan Alternatives

In summary, RV hybrid loan alternatives offer Canadian seniors versatile ways to tap home equity without the full constraints of traditional reverse mortgages. From HELOCs and no-payment hybrids to downsizing, these options balance cash flow, costs, and lifestyle preferences.

With retirement planning evolving in 2025, prioritizing low-compounding hybrids or payment-flexible products can maximize benefits. Authoritative sources like government guides underscore informed choices for long-term security.

For personalized guidance on accessing equity, consider resources at quickapprovals.ca. Evaluate your situation carefully to enjoy a comfortable retirement in your cherished home.