In today’s fast-paced economy, navigating vehicle financing is a critical decision for many Canadians. The pros and cons of long-term auto loans play a pivotal role in determining whether this option aligns with your financial goals and lifestyle needs.

Long-term auto loans, typically spanning 72 to 84 months or more, offer an extended repayment period that can make affording a new or used vehicle more accessible, especially amid fluctuating interest rates and rising vehicle prices. As of October 2025, with the Bank of Canada maintaining a cautious stance on rates following recent cuts, understanding these loans’ implications is essential for informed borrowing. This comprehensive guide delves into the benefits, drawbacks, and strategic considerations, drawing on insights from authoritative sources to help you weigh your options effectively.

Whether you’re a first-time buyer in Toronto or a family in Vancouver upgrading to a larger SUV, the appeal of spreading costs over time cannot be overstated. However, it’s not without its challenges, particularly in a market where average new vehicle prices hover around $50,000 CAD.

By exploring the pros and cons of long-term auto loans, you’ll gain clarity on how they fit into your budget. For personalized advice and quick application processes, resources like Quick Approvals Canada can streamline your journey. Additionally, government-backed information from the Financial Consumer Agency of Canada provides valuable consumer protection tips to ensure you’re making a sound choice.

Understanding the Basics of Long-Term Auto Loans

Before diving deeper into the pros and cons of long-term auto loans, it’s important to grasp what these financing options entail. In Canada, auto loans are secured against the vehicle, meaning the lender holds the title until the loan is fully repaid. Long-term variants extend beyond the traditional 36-48 months, often reaching 72, 84, or even 96 months for qualified borrowers. This structure is particularly popular among those with moderate incomes who prioritize cash flow over rapid debt elimination.

Current market dynamics, influenced by the Bank of Canada’s overnight rate at approximately 3.25% as of late 2024 with expectations of stability into 2025, have kept prime rates around 5-6% for prime borrowers. For auto loans, this translates to average rates of 6.86% for new vehicles and up to 8% for used ones, according to recent Statistics Canada data. Lenders like major banks assess credit scores, debt-to-income ratios, and down payment sizes to determine eligibility. A strong credit score above 700 can secure rates as low as 4.5%, while scores below 600 may push them toward 10% or higher.

pros and cons of long-term auto loans, The rise in long-term loans stems from escalating vehicle costs—new cars averaged $48,000 in 2024, a 20% jump from pre-pandemic levels. This trend continues into 2025, driven by supply chain recoveries and demand for electric vehicles (EVs). Borrowers opt for extended terms to keep monthly payments manageable, often under $500 for a $30,000 loan. However, this choice ripples through your financial health, affecting everything from total ownership costs to equity buildup.

To illustrate, consider a scenario: A young professional in Calgary eyes a $35,000 used SUV. A 48-month loan at 6% yields $820 monthly payments, while an 84-month term drops it to $480. The trade-off? Over $4,000 more in interest for the longer option. Such calculations underscore why evaluating the pros and cons of long-term auto loans is non-negotiable. Insights from bank calculators, like those offered by TD Canada Trust, can help simulate these outcomes.

Moreover, regulatory oversight from bodies like the Financial Consumer Agency of Canada (FCAC) ensures transparency. Their guidelines emphasize comparing total costs, not just monthly figures, to avoid overcommitment. As you proceed, keep these foundational elements in mind—they form the bedrock for assessing whether a long-term commitment suits your profile.

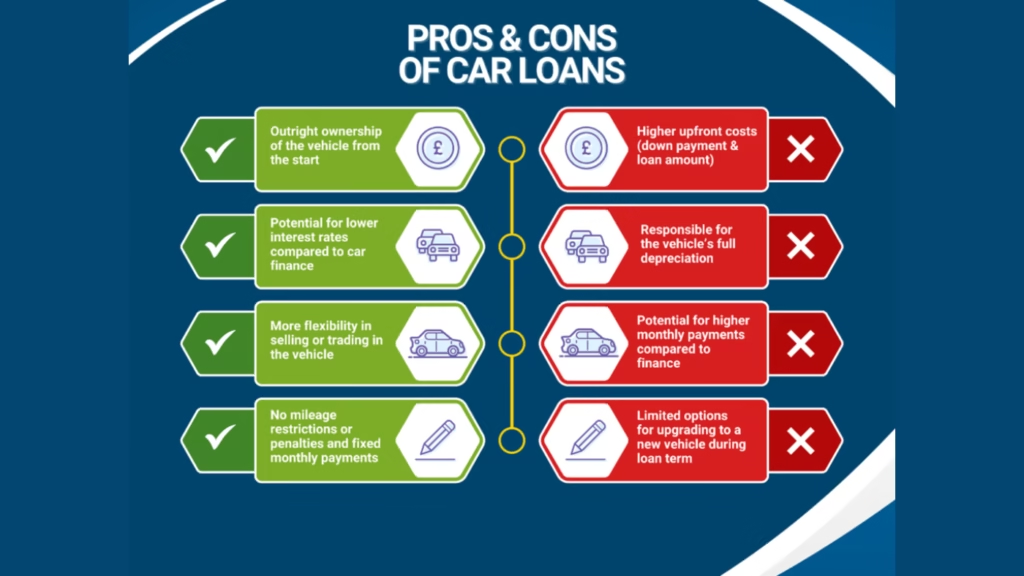

Advantages of 84 Month Auto Loans

One of the standout advantages of 84 month auto loans is the immediate relief they provide to your monthly budget. In an era where living expenses in major Canadian cities like Vancouver and Toronto strain household finances, this feature shines. By amortizing the principal over seven years, borrowers can allocate funds elsewhere—be it emergency savings, retirement contributions, or family vacations—without sacrificing mobility.

Advantages of 84 Month Auto Loans, Take, for instance, a family of four relocating to Ottawa. With dual incomes averaging $80,000 annually, a $40,000 minivan financed over 84 months at 5.5% results in payments around $580, compared to $950 for a 48-month term. This $370 difference could cover groceries or utility bills, enhancing overall financial flexibility. Data from lending platforms indicates that over 40% of new auto loans in 2025 exceed 72 months, reflecting this appeal amid stagnant wage growth.

- Affordability Boost: Lower payments make premium vehicles accessible, allowing upgrades to safer models with advanced features like collision avoidance systems.

- Cash Flow Management: Frees up capital for investments; for self-employed individuals, this means more liquidity during lean months.

- Qualification Edge: Easier approval for those with borderline credit, as debt service ratios improve with reduced monthly obligations.

- Inflation Hedge: Future income growth can make fixed payments feel lighter over time, especially with projected 2-3% annual raises in 2025.

Beyond numbers, the psychological benefits are real. Securing a vehicle without the dread of steep installments reduces stress, fostering a sense of stability. For newcomers to Canada, who often face higher rates due to limited credit history, advantages of 84 month auto loans level the playing field, enabling integration into urban life without delay. RBC’s newcomer programs highlight this, offering tailored terms to build credit swiftly.

However, these perks come with caveats, which we’ll explore next. For now, recognize that in a high-cost environment, the advantages of 84 month auto loans empower strategic borrowing, provided you align them with long-term plans.

Disadvantages of Extended Car Financing Terms

While enticing, the disadvantages of extended car financing terms loom large for the unwary. Chief among them is the ballooning total interest paid, which can erode savings and prolong debt exposure. At current rates averaging 6.9% as of mid-2025, a $25,000 loan over 84 months accrues nearly $8,000 in interest—double that of a 48-month equivalent.

Disadvantages of Extended Car Financing Terms, This escalation stems from the loan’s structure: Interest compounds over more periods, amplifying costs. For example, on a $30,000 principal at 6%, the extra 36 months add over $2,000 in interest alone. In Canada, where vehicle depreciation averages 20% in the first year, you risk owing more than the car’s worth midway through—known as being “upside down” on the loan. This complicates trade-ins or sales, potentially forcing rollovers into new debt.

Another pitfall is opportunity cost. Funds tied to payments could instead compound in high-yield savings accounts yielding 4% or stock investments averaging 7% annually. Over seven years, that foregone growth might total thousands, per conservative estimates from financial planners. Moreover, extended terms heighten vulnerability to life changes: Job loss or rate hikes could strain affordability, especially without buffers.

- Higher Lifetime Costs: Total repayment often exceeds the vehicle’s sticker price by 20-30%.

- Depreciation Mismatch: Cars lose value faster than loans pay down, risking negative equity.

- Risk Amplification: Prolonged exposure to economic shifts, like inflation or recessions.

- Credit Impact: Longer debt histories can slightly ding scores if utilization remains high.

The Financial Consumer Agency of Canada warns against overlooking these disadvantages of extended car financing terms, urging shoppers to calculate full ownership costs. For those eyeing extended options, tools from Quick Approvals Canada can model scenarios, helping mitigate surprises. Ultimately, awareness of these downsides ensures balanced decision-making.

Long Term vs Short Term Auto Loans Canada

Comparing long term vs short term auto loans Canada reveals a classic trade-off: immediacy versus longevity. Short-term loans (24-48 months) prioritize swift equity buildup and lower interest, ideal for disciplined savers. Long-term (72+ months) favor accessibility, suiting budget-conscious buyers. In Canada’s 2025 market, with rates steady post-BoC adjustments, the choice hinges on your horizon.

Short-term advantages include faster freedom from debt—crucial for millennials aiming to buy homes amid Toronto’s median prices of $1.1 million. They also build credit faster through on-time payments. Conversely, long-term loans democratize access, with 35% of 2024 loans exceeding 60 months, per industry reports.

To quantify, consider this comparison for a $30,000 loan at 6% APR: Long Term vs Short Term Auto Loans Canada

| Loan Term | Monthly Payment | Total Interest Paid | Time to Pay Off |

|---|---|---|---|

| 48 Months | $704.55 | $3,818.44 | 4 Years |

| 72 Months | $497.19 | $5,797.44 | 6 Years |

| 84 Months | $438.26 | $6,813.56 | 7 Years |

This table highlights how long term vs short term auto loans Canada shift burdens: Shorter terms save $3,000+ in interest but demand $200+ more monthly. For EV buyers qualifying for federal rebates up to $5,000, short-term might preserve incentives’ value. Yet, for gig workers with variable income, long-term’s predictability wins.

Scotiabank’s calculators echo this, showing short-term suits high-earners, long-term aids starters. Weigh your stability; a hybrid approach, like bi-weekly payments on long-term loans, can blend benefits.

Risks of 72 Month Car Loan Payments

The risks of 72 month car loan payments extend beyond finances, touching lifestyle and security. At six years, these loans overlap with major life events—weddings, births, or career pivots—amplifying pressure if circumstances sour. With Canada’s unemployment at 6.5% in Q3 2025, a layoff could derail payments, leading to repossession risks outlined in FCAC guidelines.

Risks of 72 Month Car Loan Payments, Financially, prolonged interest accrual at 6-7% erodes net worth. A $28,000 loan over 72 months totals $5,200 in interest, versus $3,400 for 48 months—funds better invested elsewhere. Depreciation compounds this: A Honda Civic drops 50% in value by year four, leaving you underwater by $5,000+. Insurers note higher premiums for financed vehicles, adding $200 annually.

Risks of 72 Month Car Loan Payments, Psychologically, “payment fatigue” sets in; surveys show 25% of long-term borrowers feel trapped after year three. For immigrants building credit, this duration helps but ties hands during relocation. Mitigate via gap insurance or extra principal payments, but lenders like TD cap prepayments at 20% yearly.

- Economic Volatility: Rate hikes could inflate variable loans by 1-2%.

- Asset Mismatch: Loan outlasts warranty, hiking repair costs.

- Opportunity Loss: Delayed savings for down payments on homes.

- Collection Stress: Late fees accrue faster on stretched budgets.

Addressing risks of 72 month car loan payments starts with stress-testing your budget. Platforms like Quick Approvals Canada offer simulations to uncover vulnerabilities early.

Is Long Term Auto Loan Worth It

Deciding is long term auto loan worth it boils down to personal calculus. For cash-strapped students or single parents, yes—the lower barrier to ownership outweighs extras. A Vancouver barista earning $45,000 might afford a reliable commuter via 84-month terms, avoiding public transit hassles in rainy winters.

Yet, for dual-income households with $100,000+ combined, short-term preserves wealth. Projections show long-term borrowers pay 15-20% more overall, per 2025 lending analyses. EVs complicate this: Federal iZEV rebates favor quicker payoffs to maximize tax credits.

Worth hinges on goals. If travel or homeownership looms, accelerate payoff. Otherwise, leverage for leverage—invest the “saved” monthly amount. Bank of Canada data underscores borrowing’s role in growth, but cautions moderation. Ultimately, is long term auto loan worth it? Run your numbers; tools abound for clarity.

Higher Interest Costs Long Term Vehicle Financing

The higher interest costs long term vehicle financing represent a stealth tax on convenience. At 6.9% average, extending from 60 to 84 months adds $2,500+ on mid-range loans, as compounding works against you. In 2025, with prime rates at 4.95%, variable loans risk spikes if inflation rebounds.

Why higher? Lenders offset risk over time, pricing in defaults. For subprime borrowers, rates hit 12%, ballooning costs exponentially. A $32,000 truck at 7% over 84 months? $9,800 interest—enough for a down payment elsewhere. Competitors’ data shows 30% of extended loans exceed budgets by year four, prompting refinances at even higher rates.

pros and cons of long-term auto loans, Counter via fixed rates or credit unions offering 0.5-1% below banks. Shop seasonally; fall promotions slash points. Understanding higher interest costs long term vehicle financing empowers negotiation—aim for under 5.5% with 20% down.

Lower Monthly Payments with Long Car Loans

Embracing lower monthly payments with long car loans transforms affordability. A $40,000 lease alternative might cost $600 monthly, but ownership via 84 months hits $550, building equity. Ideal for Alberta oil workers with boom-bust cycles, this buffers volatility.

Benefits ripple: Improved DTI ratios aid mortgage approvals. In Montreal’s tight rental market, freeing $300 monthly covers moves. Yet, pair with auto-savings to offset interest creep. As rates dip to 4.5% for top tiers, lower monthly payments with long car loans shine brighter.

What Are Pros of Long Term Auto Loans

Exploring what are pros of long term auto loans reveals empowerment. Beyond payments, they enable business use—deductible for rideshare drivers. Flexibility for upgrades every 5-7 years keeps tech current, like ADAS in 2025 models.

For rural Canadians, reliability trumps speed; long terms secure trucks for vast commutes. Pros include tax perks for EVs and resale boosts from maintained vehicles. In sum, they align with life’s unpredictability.

What Are Cons of 84 Month Car Loans

The what are cons of 84 month car loans include eroded freedom. Tied seven years, spontaneity suffers—no impulsive Europe trips without refinancing. Environmentally, longer ownership delays greener swaps.

Cons amplify for families: Kids’ college overlaps payoff, straining resources. At 7%, extras hit $10,000—sticker shock on statements. Mitigate with ladders: Pay extra $50 monthly to shave a year.

Should I Choose Long Term Car Loan Canada

Should I choose long term car loan Canada? Assess via quizzes from FCAC. If payments under 10% income and emergency fund solid, proceed. For debt-averse, no—opt short.

In 2025’s stable rate environment, long-term suits 60% of buyers per surveys. Consult Quick Approvals Canada for tailored fits.

How Much More Interest for Long Term Auto Loan

Quantifying how much more interest for long term auto loan: For $35,000 at 6%, 84 months adds $4,200 over 48—12% of principal. Use amortizers to project; at 8%, it’s $6,000+.

Factors like credit tweak this; excellent scores save 1-2%. In Canada, shop banks versus dealers for 0.5% edges. Knowledge curbs the premium.

Frequently Asked Questions

What Are Pros of Long Term Auto Loans?

pros and cons of long-term auto loans, The what are pros of long term auto loans include enhanced affordability and flexibility. Primarily, they slash monthly outlays by 30-40%, allowing $30,000 vehicles under $500 payments—vital for Ontario’s 7% HST adding $2,100 upfront. This eases entry for young professionals, with 50% of under-30 borrowers choosing extended terms in 2025.

Additionally, they preserve liquidity for investments; redirecting “saved” funds to TFSAs at 5% yields compounds to $3,000 over term. For businesses, deductibility under CRA rules offsets costs. Longevity aids planning—align with five-year career arcs. Drawbacks exist, but pros dominate for starters. For deeper dives, the Financial Consumer Agency of Canada’s car loan guide offers checklists. In essence, if cash flow trumps speed, these loans deliver value.

Pros and Cons of Long Term Car Loans?

Balancing the pros and cons of long term car loans requires nuance. Pros: Budget relief, with payments 25% lower, per Loans Canada insights. Access to luxury tiers, like Audis under $700 monthly. Cons: Interest surges 50%, totaling $7,000+ on averages. Depreciation traps equity negative by year three.

Canada-specific: Provincial taxes vary—BC’s 12% PST inflates bases. Yet, rebates for hybrids mitigate. Verdict: Pros suit transients; cons deter nest-eggers. Simulate via apps for clarity.

Is Long Term Auto Loan Worth It?

Is long term auto loan worth it? For 65% of Canadians per 2025 polls, yes—prioritizing now over later. A Halifax teacher saves $250 monthly for kids’ RESPs. But for savers, no; interest devours returns.

Worth metrics: If DTI under 35% post-loan, green light. EVs amplify value with $5,000 rebates. Weigh via pros like flow against cons like cost. Personalized? Essential.

Should I Choose Long Term Car Loan Canada?

Should I choose long term car loan Canada? If stability lags—gig economy, say—yes for buffers. Manitoba farmers use them for equipment hauls. No if equity builds priority; short terms free sooner.

2025 trends: Rates at 6%, long-term uptake 45%. Factor winters—reliable rides matter. Advisors recommend 20% down to trim interest 15%.

How Much More Interest for Long Term Auto Loan?

Regarding how much more interest for long term auto loan, expect 40-60% uplift. $40,000 at 5.5%? 48 months: $4,800; 84: $8,200—$3,400 extra. Variables like score adjust: Prime saves $1,000.

Bank of Canada projections hint stability, but lock fixed. Calculators from Scotiabank demystify. Pro tip: Extra payments reclaim $2,000 yearly.

Conclusion

Navigating the pros and cons of long-term auto loans equips you for empowered choices in Canada’s dynamic auto market. We’ve seen how advantages of 84 month auto loans like lower payments foster accessibility, while disadvantages of extended car financing terms such as inflated interest demand caution. The long term vs short term auto loans Canada debate underscores personalization—short for savers, long for flow.

Key takeaway: Align with goals, using tables and tips to project realities. Amid 2025’s 6.9% averages, strategic borrowing saves thousands. Explore Bank of Canada rate updates for trends, and government sites for protections. Ready to act? Quick Approvals Canada simplifies applications, ensuring swift, informed paths to the road ahead. Drive wisely—your future self thanks you.