In Canada, securing a car loan with high debt-to-income ratio Canada can feel like an uphill battle, especially with rising household debt levels and stricter lending standards. The debt-to-income (DTI) ratio, which measures your monthly debt payments against your income, is a critical factor lenders use to assess your ability to manage new loans. A high DTI—typically above 36%—signals financial strain, making loan approval challenging. However, with the right strategies and knowledge, Canadians can still access car financing.

This article explores how to navigate car loan with high debt-to-income ratio Canada, offering practical tips, lender insights, and actionable steps to improve your approval odds, all while leveraging authoritative resources like those from the Financial Consumer Agency of Canada (FCAC).

Understanding How to Get a Car Loan with High Debt to Income Ratio in Canada

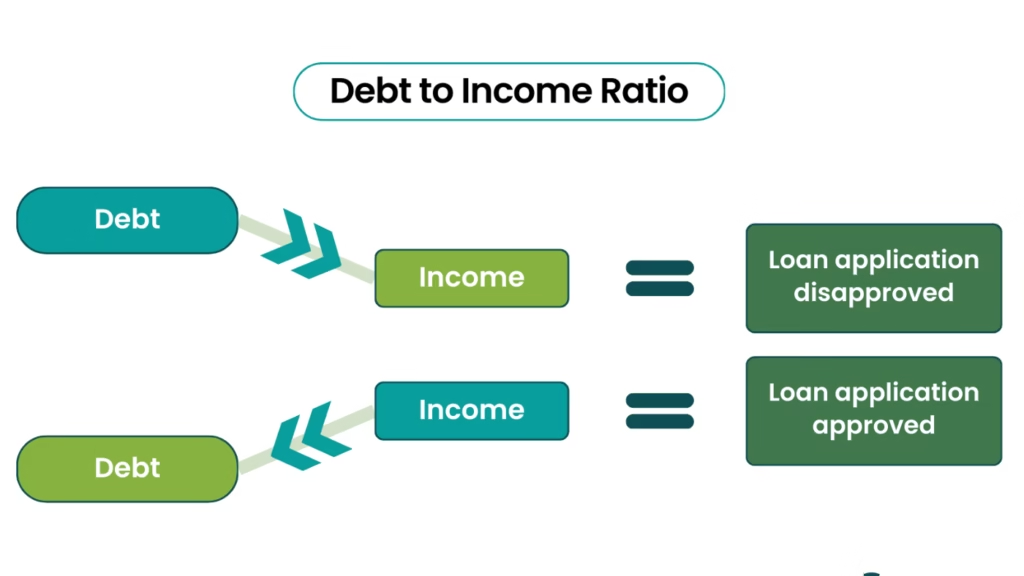

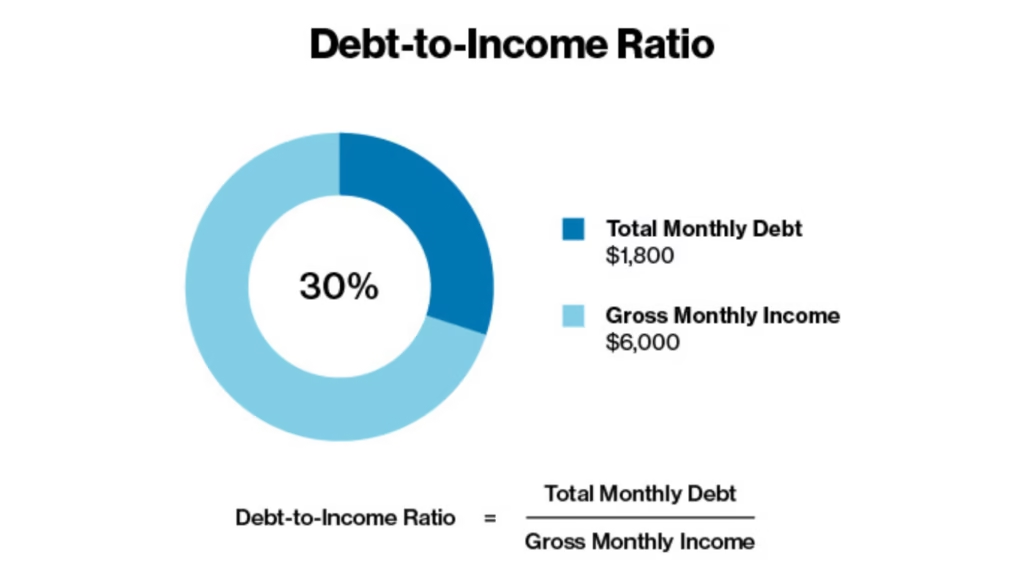

car loan with high debt-to-income ratio Canada, The DTI ratio is calculated by dividing your total monthly debt payments (e.g., credit cards, mortgages, student loans) by your gross monthly income. For example, if your monthly debt payments are $2,000 and your gross income is $5,000, your DTI is 40%. Lenders in Canada prefer a DTI below 36%, but some may approve car loans with high DTI Canada with additional conditions, such as higher interest rates or a co-signer.

Lenders assess DTI to gauge repayment risk. A high DTI suggests limited financial flexibility, but approval is still possible through specialized lenders or by improving your financial profile. Here are key factors lenders consider:

- Credit Score: A strong credit score (above 670) can offset a high DTI, showing responsible credit management.

- Income Stability: Consistent employment or income sources reassure lenders of repayment ability.

- Down Payment: A larger down payment reduces the loan amount, lowering risk for lenders.

- Collateral: Secured loans, where the car serves as collateral, are easier to obtain with high DTI.

Exploring options through platforms like Quick Approvals can connect you with lenders who specialize in car loan approval with high DTI Canada

Strategies to Secure Car Loan Approval with High DTI Canada

Achieving car loan approval with high DTI Canada requires strategic planning. Lenders may hesitate, but specific actions can improve your chances. Below are proven strategies to strengthen your application:

- Pay Down Existing Debt: Reducing credit card balances or small loans lowers your DTI, making you a stronger candidate.

- Increase Income: Supplement your income with part-time work or side gigs to improve your DTI ratio.

- Choose a Cheaper Vehicle: Opting for a lower-priced car reduces the loan amount, easing lender concerns.

- Get a Co-Signer: A co-signer with good credit and low DTI can bolster your application.

- Shop Around: Compare offers from banks, credit unions, and online lenders specializing in high-DTI loans.

According to the FCAC, understanding loan terms and comparing lenders is crucial for informed decisions. Platforms like Quick Approvals can streamline this process, matching you with lenders suited to your financial situation.

How to Lower DTI for Car Loan Approval in Canada

Lowering your DTI is one of the most effective ways to improve your eligibility for a car loan with high debt-to-income ratio Canada. Here’s a step-by-step guide to reducing your DTI:

| Action | Impact on DTI | Timeframe |

|---|---|---|

| Pay off high-interest credit cards | Reduces monthly debt payments | 1-3 months |

| Consolidate loans | Lowers monthly payments by extending terms | Immediate |

| Increase income (e.g., freelance work) | Boosts denominator in DTI calculation | 1-6 months |

| Avoid new debt | Prevents DTI from rising | Ongoing |

Debt consolidation, for instance, can combine multiple debts into a single payment with a lower interest rate, directly impacting improving debt to income ratio for car loan Canada. Consult with financial advisors or use online tools to track progress.

Exploring Best Car Loans for High Debt to Income Ratio Canada

Not all lenders treat high DTI applicants the same. Some specialize in best car loans for high debt to income ratio Canada, offering flexible terms. Credit unions, for example, often have more lenient criteria than major banks like RBC or TD. Online lenders and dealership financing programs also cater to high-DTI borrowers, though interest rates may be higher.

Key features to look for in these loans include:

- Flexible repayment terms (e.g., 60-84 months).

- Pre-approval options to lock in rates without impacting credit.

- Low or no prepayment penalties for early repayment.

Researching lenders that approve car loans with high DTI Canada can uncover niche providers. Platforms like Quick Approvals simplify this by connecting you with vetted lenders.

Car Financing Options for High Debt Ratio in Canada

Beyond traditional loans, **_car financing options for high debt ratio in Canada_** include alternatives like leasing or personal loans. Leasing often requires a lower DTI since monthly payments are typically lower than loan payments. However, you don’t own the vehicle at the end of the term. Personal loans, while unsecured, may be viable for those with strong credit despite high DTI, though they often carry higher interest rates.

Another option is **_alternatives to car loans with high DTI in Canada_**, such as borrowing from family or using savings for a cash purchase. These avoid debt entirely but may not be feasible for everyone.

Addressing Bad Credit Car Loans with High DTI Canada

A high DTI often pairs with poor credit, complicating financing. **_Bad credit car loans with high DTI Canada_** are offered by subprime lenders who focus on credit-challenged borrowers. These loans come with higher interest rates (often 10-20%) and stricter terms, but they provide a pathway to vehicle ownership.

To improve approval odds:

- Provide proof of stable income.

- Offer a substantial down payment (20% or more).

- Work with lenders specializing in subprime loans.

Improving your credit score over time can also open doors to better terms, complementing efforts in **_improving debt to income ratio for car loan Canada_**.

Tips for Getting Car Loan with High DTI in Canada

Securing a car loan with high debt-to-income ratio Canada demands preparation. Here are actionable tips for getting car loan with high DTI in Canada:

- Check Your Credit Report: Dispute errors to boost your score.

- Save for a Down Payment: Aim for 10-20% to reduce lender risk.

- Negotiate Loan Terms: Seek lower rates or extended terms to ease payments.

- Avoid Overborrowing: Stick to a budget to prevent further DTI strain.

Using platforms like Quick Approvals can help you find lenders aligned with these strategies.

Q&A: Common Questions About Car Loan with High Debt-to-Income Ratio Canada

1. Can I Get a Car Loan with High DTI in Canada?

Yes, approval is possible, but it depends on the lender. Specialized lenders, such as those found through Quick Approvals, focus on car loan approval with high DTI Canada. A strong credit score, stable income, or co-signer can improve your chances. The FCAC advises comparing lenders to find favorable terms.

2. What Is the Maximum DTI for Car Loans in Canada?

Most lenders prefer a DTI below 36%, but some accept up to 43-50% for car loans with high DTI Canada. Subprime lenders may go higher, but interest rates increase. Check with lenders directly to confirm their thresholds.

3. How to Lower DTI for Car Loan Approval in Canada?

Lowering DTI involves reducing debt or increasing income. Pay off high-interest debts, consolidate loans, or take on freelance work. The FCAC offers tools for debt management to support improving debt to income ratio for car loan Canada.

4. Who Are the Lenders That Approve Car Loans with High DTI Canada?

Credit unions, online lenders, and some dealerships specialize in lenders that approve car loans with high DTI Canada. Examples include Canada Drives and subprime divisions of major banks. Always review terms to avoid predatory rates.

5. What Are Alternatives to Car Loans with High DTI in Canada?

Alternatives include leasing, personal loans, or borrowing from family. Leasing often has lower monthly payments, easing DTI concerns. Cash purchases avoid debt but require significant savings. Explore these alternatives to car loans with high DTI in Canada based on your financial goals.

Conclusion

Navigating a car loan with high debt-to-income ratio Canada requires understanding your DTI, exploring flexible lenders, and improving your financial profile. By lowering debt, boosting income, or opting for alternatives like leasing, Canadians can overcome high-DTI challenges. Resources like the Financial Consumer Agency of Canada provide valuable guidance, while platforms like Quick Approvals connect you with tailored financing options. Take proactive steps, compare lenders, and make informed decisions to secure your next vehicle.