The landscape of automotive financing in Canada is ever-changing, with car loan rate trends in Canada playing a pivotal role in how consumers approach vehicle purchases. Whether you’re eyeing a new SUV or a fuel-efficient sedan, understanding these trends is crucial for making informed financial decisions.

car loan rate trends in Canada, Interest rates on car loans are influenced by economic factors, lender policies, and market dynamics, impacting monthly payments and overall loan costs. For the latest insights and personalized options, visit Quick Approvals, a resource for navigating Canada’s auto financing landscape. This article dives deep into the factors driving these trends, practical tips for securing favorable rates, and answers to common questions, supported by authoritative data from sources like the Bank of Canada.

Current Car Loan Interest Rates Canada: What to Expect

car loan rate trends in Canada, The current car loan interest rates Canada are shaped by the Bank of Canada’s overnight rate, inflation, and lender competition. As of 2025, rates for new car loans typically range from 4.5% to 8%, depending on credit scores, loan terms, and whether the vehicle is new or used. Borrowers with excellent credit (700+) may secure rates as low as 4.5%, while those with lower scores might face rates closer to 8% or higher.

Fixed-rate loans dominate the market, offering predictability, though variable-rate loans can be attractive when rates are expected to decline. For instance, recent economic cooling has led some lenders to offer promotional rates to attract buyers, especially for electric vehicles (EVs).

- Credit Score Impact: A credit score above 700 often unlocks lower rates, while scores below 600 may push rates above 7%.

- Loan Term: Shorter terms (e.g., 36 months) usually have lower rates than longer terms (e.g., 72 months).

- Lender Type: Banks like RBC and TD compete with credit unions and manufacturer financing (e.g., Toyota Financial), which may offer 0% promotional rates.

Data from sites like Ratehub indicates that major banks adjust rates in response to Bank of Canada policies, with recent rate hikes in 2023-2024 pushing averages up slightly. However, competition among lenders keeps rates accessible for qualified buyers.

Exploring Average Car Loan Rates Canada 2025

The average car loan rates Canada 2025 reflect a balance between economic recovery and cautious lending. According to industry insights, the average rate for a 60-month new car loan hovers around 5.5% for prime borrowers. Used car loans tend to carry higher rates, averaging 6.5% to 8%, due to perceived risk. These averages fluctuate based on:

- Economic Indicators: Inflation and employment rates influence lender confidence.

- Vehicle Type: EVs and hybrids often qualify for lower rates due to government incentives.

- Seasonal Promotions: Dealerships may offer lower rates in spring or fall to clear inventory.

For real-time rate comparisons, tools like Quick Approvals can streamline the process, connecting you with lenders offering competitive terms tailored to your needs.

Finding the Best Car Loan Rates Canada Today

Securing the best car loan rates Canada today requires strategic planning. Start by shopping around, as rates vary significantly between banks, credit unions, and dealership financing. Credit unions, for example, often provide lower rates to members, sometimes as low as 4% for strong credit profiles. Manufacturer financing, such as Ford Credit or GM Financial, occasionally offers 0% APR for specific models, though these deals often require shorter loan terms or higher down payments.

Here’s a quick comparison of lender types based on industry data:

| Lender Type | Typical Rate Range | Pros | Cons |

|---|---|---|---|

| Major Banks | 5.0%–7.5% | Wide availability | Stricter credit requirements |

| Credit Unions | 4.0%–6.5% | Lower rates for members | Membership required |

| Dealership Financing | 0%–8% | Promotional offers | Limited to specific models |

Tips to secure the best rates include improving your credit score, opting for a shorter loan term, and making a larger down payment (20% or more). Checking platforms like Loans Canada for pre-approval options can also help lock in favorable terms.

Analyzing Car Loan Rate Trends Canada 2025

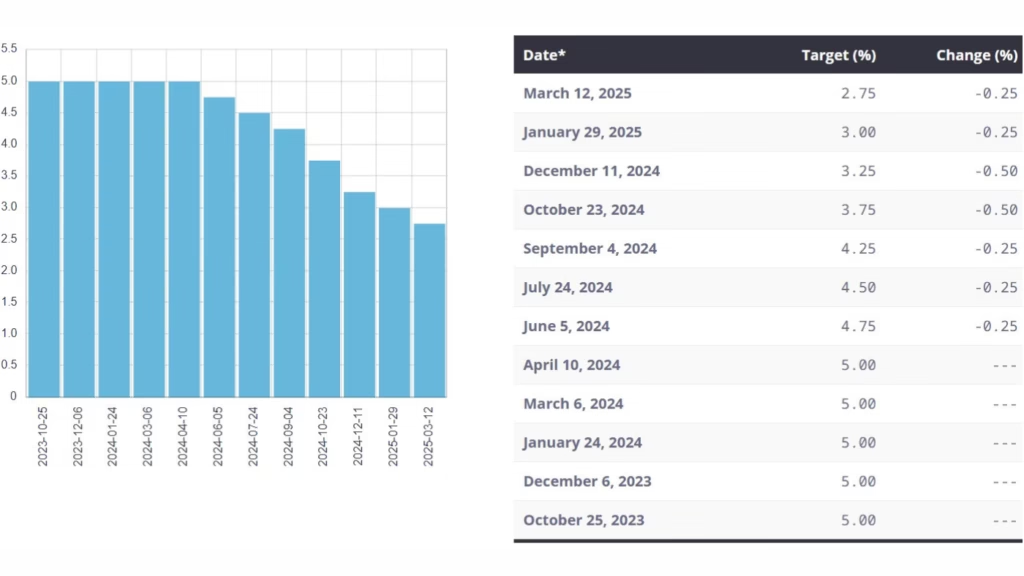

The car loan rate trends Canada 2025 are influenced by macroeconomic shifts. The Bank of Canada’s monetary policy, accessible via their official rates page, sets the tone for lending rates. After a series of rate hikes in 2023-2024 to combat inflation, 2025 shows signs of stabilization, with potential rate cuts if inflation remains below 2%. This could lower car loan rates, especially for variable-rate loans. Additionally, government incentives for EVs are pushing lenders to offer competitive rates for eco-friendly vehicles, a trend likely to continue as Canada aims for net-zero emissions by 2050.

Seasonal trends also play a role. Data from AutoTrader suggests that spring and fall are peak times for car purchases, prompting lenders to offer promotional rates. For example, rates may dip by 0.5%–1% during these periods to attract buyers.

How to Compare Car Loan Rates Canadian Banks

To effectively **_compare car loan rates Canadian banks_**, focus on APR (Annual Percentage Rate), which includes interest and fees. Major banks like Scotiabank and BMO provide online calculators to estimate monthly payments, but you’ll need to request personalized quotes for accurate rates. Credit unions, such as Vancity or Meridian, often beat bank rates by 0.5%–1% for members. Here’s how to approach comparisons:

- Request Multiple Quotes: Contact at least three lenders to compare offers.

- Check Pre-Approval: Pre-approval locks in rates without impacting your credit score.

- Read Fine Print: Look for hidden fees, such as prepayment penalties.

Resources like Quick Approvals simplify this process by aggregating offers from multiple lenders, saving time and effort.

Factors Affecting Car Loan Rates Canada

Several factors affecting car loan rates Canada determine the rates you’re offered. Understanding these can help you negotiate better terms:

- Credit Score: Higher scores (700+) secure lower rates; scores below 600 may face rates above 8%.

- Loan Term: Shorter terms (36–48 months) typically have lower rates than longer ones (72–84 months).

- Vehicle Age: New cars often qualify for lower rates than used cars.

- Economic Conditions: Bank of Canada rate changes directly impact loan rates.

- Down Payment: A larger down payment (20%+) reduces lender risk, lowering rates.

Insights from LowestRates.ca highlight that borrowers with strong credit and larger down payments can save thousands over the loan term by securing rates 1%–2% lower than average.

Q&A: Common Questions About Car Loan Rate Trends in Canada

What Are Current Car Loan Rates Canada?

The **_current car loan rates Canada_** typically range from 4.5% to 8% for new cars and 6% to 10% for used cars, based on credit profiles and loan terms. For precise rates, check with lenders like RBC or use platforms like Quick Approvals to compare offers. The Bank of Canada’s overnight rate, detailed on their rates page, influences these figures, with recent stabilization suggesting steady or slightly declining rates in 2025.

How to Get Lowest Car Loan Rate Canada?

To get the **_how to get lowest car loan rate Canada_**, improve your credit score, shop multiple lenders, and consider a larger down payment. Pre-approval is key, as it locks in rates without credit score damage. Credit unions and promotional dealership offers often provide the lowest rates, sometimes as low as 0% for specific models. Comparing offers through resources like Quick Approvals can help identify the best deals.

Why Are Car Loan Rates Rising Canada?

**_Why are car loan rates rising Canada_**? Recent increases stem from Bank of Canada rate hikes in 2023-2024 to curb inflation, which raised borrowing costs for lenders. Global supply chain issues and higher vehicle prices also contribute, as lenders adjust rates to mitigate risk. However, stabilization in 2025 may ease upward pressure, especially for EV loans incentivized by government policies.

Is Now Good Time Car Loan Canada?

Deciding if **_is now good time car loan Canada_** depends on your financial situation and market trends. With rates stabilizing in 2025, it’s a reasonable time for borrowers with strong credit, especially for EVs with promotional rates. However, if rates are expected to drop further, waiting a few months could yield savings. Use tools like Quick Approvals to monitor current offers.

How Do car loan rate trends Canada 2025 Affect Buyers?

The car loan rate trends Canada 2025 impact affordability. Stable or slightly declining rates mean predictable payments, but borrowers with lower credit scores may still face higher rates (7%+). EV buyers may benefit from lower rates due to incentives, while used car buyers could see higher rates due to vehicle age. Staying informed via the Bank of Canada’s website helps anticipate shifts.

Conclusion

The car loan rate trends in Canada are a critical factor for anyone planning to finance a vehicle in 2025. From understanding current car loan interest rates Canada to navigating factors affecting car loan rates Canada, informed decisions can save thousands over the loan term. By comparing offers, improving credit, and leveraging seasonal promotions, buyers can secure the best car loan rates Canada today. For further insights, explore authoritative resources like the Bank of Canada and connect with trusted platforms like Quick Approvals to find tailored financing options. Stay proactive, compare rates, and drive away with confidence.