Canada’s auto financing market has evolved significantly over the last decade. Behind the scenes of many vehicle loans lies a sophisticated financial process known as auto loan securitization Canada. While most borrowers focus on monthly payments, loan terms, and approval requirements, lenders and investors often rely on securitization to maintain funding capacity and support continued lending activity.

Understanding auto loan securitization Canada helps consumers gain insight into how lenders fund vehicle loans, why financing remains widely available, and how financial institutions manage lending risks. This process plays a major role in creating liquidity within the automotive finance sector while supporting the availability of competitive financing products across the country.

Whether you are applying for vehicle financing, researching lending trends, or simply seeking a deeper understanding of Canada’s automotive credit market, this guide explains the complete securitization process, eligibility considerations, costs, risks, opportunities, and future developments.

What Is Auto Loan Securitization Canada?

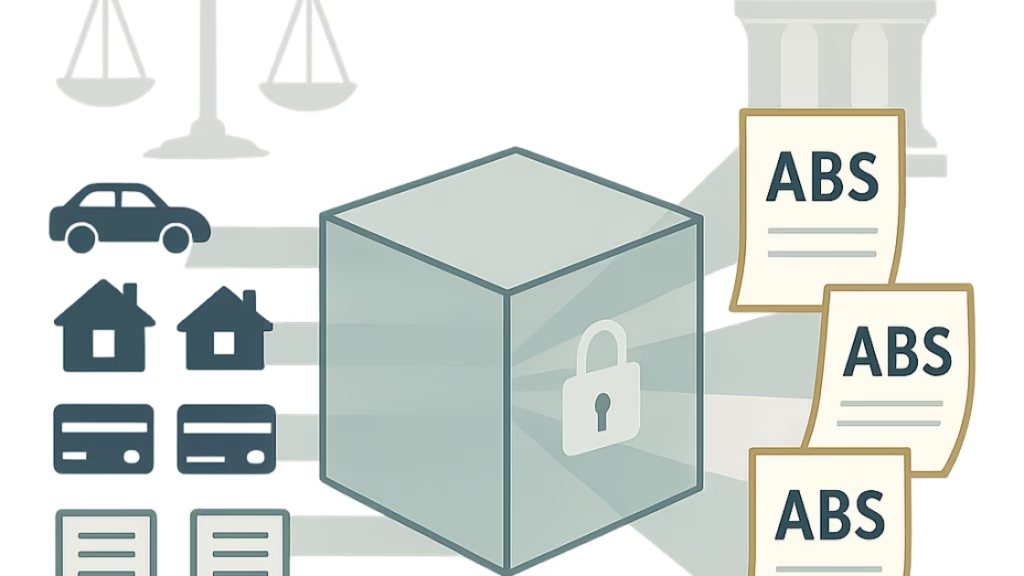

Auto loan securitization Canada refers to the process through which lenders bundle multiple vehicle loans together and convert them into tradable financial securities that can be sold to investors.

Instead of waiting several years to collect monthly payments from borrowers, lenders package hundreds or thousands of auto loans into investment products. These securities generate income from borrower repayments and are purchased by institutional investors seeking predictable cash flow. Through this process, lenders receive immediate capital that can be used to issue additional vehicle loans across Canada.

The system benefits multiple participants: auto loan securitization Canada

- Consumers gain access to financing.

- Lenders improve liquidity.

- Investors access diversified income-producing assets.

- Financial markets increase efficiency.

As Canada’s vehicle financing market continues growing, securitization remains one of the most important funding mechanisms supporting automotive lending activity. auto loan securitization Canada

Understanding Asset Backed Car Loans Canada

The foundation of securitization begins with asset backed car loans Canada. These are vehicle loans secured by the financed automobile itself.

When borrowers make monthly payments, those payments become future cash flows. Financial institutions group thousands of these cash flows into portfolios that serve as collateral for asset-backed securities.

Key characteristics include:

Vehicle Assets Support the Investment

Unlike unsecured lending products, vehicle loans are tied to tangible assets. If borrowers default, lenders may recover a portion of losses through repossession and resale of the vehicle.

Diversified Loan Pools

Securitization structures typically include large numbers of loans from different provinces, borrowers, vehicle types, and credit profiles. Diversification helps reduce concentration risk.

Predictable Payment Streams

Most vehicle loans follow fixed monthly repayment schedules, creating stable income streams that investors generally find attractive.

Risk Distribution

Rather than holding all loan risk internally, lenders distribute portions of that risk among institutional investors participating in the securitization market. Asset Backed Car Loans Canada

How Securitized Auto Finance Canada Works Step by Step

Understanding securitized auto finance Canada becomes easier when viewed as a structured process.

Step 1: Loan Origination

Banks, credit unions, captive finance companies, and alternative lenders approve vehicle financing for consumers.

Borrowers purchase:

- New vehicles

- Used vehicles

- SUVs

- Pickup trucks

- Commercial vehicles

Each loan creates a future stream of scheduled payments.

Step 2: Portfolio Creation

The lender accumulates thousands of active vehicle loans.

The portfolio may contain:

- Prime borrowers

- Near-prime borrowers

- Different loan terms

- Various vehicle values

- Geographic diversification

This creates a balanced lending pool.

Step 3: Special Purpose Vehicle Formation

The lender transfers the loan portfolio into a separate legal entity commonly known as a Special Purpose Vehicle (SPV).

The SPV becomes responsible for issuing securities backed by the loan assets.

Step 4: Security Issuance

The SPV creates investment products supported by expected borrower repayments.

Institutional investors purchase these securities and provide capital to the SPV.

Step 5: Cash Flow Distribution

Borrowers continue making monthly payments.

Funds flow through the SPV and are distributed to investors according to the terms of the security structure.

Step 6: Ongoing Monitoring

Loan performance, delinquency rates, defaults, and recoveries are continuously monitored to ensure investment quality and regulatory compliance. Securitized Auto Finance Canada

Why Institutional Investment Car Loans Canada Matter

The success of Canada’s auto finance market depends heavily on institutional investment car loans Canada.

Institutional investors commonly include:

- Pension funds

- Insurance companies

- Asset managers

- Investment funds

- Financial institutions

These investors seek stable income-generating assets that offer predictable returns while maintaining diversification.

Benefits include: Institutional Investment Car Loans Canada

Increased Lending Capacity

Investor funding allows lenders to continue issuing vehicle loans without relying solely on deposits or internal capital.

Enhanced Market Liquidity

Securitization converts long-term loans into liquid capital, supporting financial market efficiency.

Competitive Financing Availability

Greater funding access often supports broader lending opportunities for qualified borrowers.

Risk Management

Institutions can allocate exposure across various asset classes instead of concentrating risk in a single area. Institutional Investment Car Loans Canada

Key Components of Canadian Auto Loan Asset-Backed Securities

Several important elements determine the structure and performance of securitized vehicle financing products.

Loan Pool Quality

The quality of the underlying vehicle loans significantly influences investor confidence.

Important factors include:

- Borrower credit profiles

- Payment history

- Loan-to-value ratios

- Vehicle age

- Delinquency trends

Credit Enhancement

Many securitization structures include safeguards designed to absorb potential losses.

Examples include:

- Reserve accounts

- Overcollateralization

- Subordination structures

These protections improve investment stability.

Servicing Quality

Loan servicing companies manage:

- Payment collection

- Customer support

- Delinquency management

- Reporting

Strong servicing standards contribute to portfolio performance.

Economic Conditions

Employment levels, interest rates, inflation, and vehicle market conditions all influence repayment performance.

Benefits of Canadian Auto Loan ABS Trends Canada for Borrowers

Although securitization occurs behind the scenes, borrowers can still experience several indirect benefits resulting from Canadian auto loan ABS trends Canada.

Greater Financing Availability

Lenders with strong securitization programs often have access to larger funding sources, enabling them to approve more applications.

Expanded Vehicle Options

Consumers may find financing opportunities for a broader range of vehicles and borrower profiles.

Market Stability

Efficient funding mechanisms support continuous lending activity even during changing economic cycles.

Product Innovation

Competitive funding environments often encourage lenders to develop more flexible financing solutions.

Faster Lending Decisions

Improved liquidity allows many lenders to streamline approval systems and accelerate funding timelines. Canadian Auto Loan ABS Trends Canada

Eligibility Requirements for Auto Loans Included in Securitization Pools

Not every vehicle loan automatically qualifies for securitization programs.

Lenders typically evaluate several factors.

| Requirement | Typical Consideration |

|---|---|

| Credit Profile | Borrower repayment history |

| Income Stability | Consistent employment or income |

| Vehicle Value | Appropriate collateral value |

| Loan Term | Structured repayment schedule |

| Documentation | Complete verification records |

| Payment History | Strong ongoing performance |

High-quality loan portfolios generally attract stronger investor demand.

Interest Rates and Cost Breakdown

Although securitization itself does not directly determine borrower rates, several factors influence overall financing costs.

| Factor | Impact on Borrower |

|---|---|

| Credit Score | Strong influence |

| Income Stability | Moderate influence |

| Vehicle Age | Moderate influence |

| Loan Term | Significant influence |

| Down Payment | May lower risk |

| Market Conditions | Influences lender pricing |

Example 1: Prime Borrower

Vehicle Price: $35,000

Down Payment: $5,000

Loan Amount: $30,000

Term: 60 Months

Estimated Rate: 5.99%

Monthly Payment: Approximately $580

Total Interest: Approximately $4,800

Example 2: Near-Prime Borrower

Vehicle Price: $28,000

Down Payment: $3,000

Loan Amount: $25,000

Term: 72 Months

Estimated Rate: 8.99%

Monthly Payment: Approximately $451

Total Interest: Approximately $7,472

Example 3: Alternative Lending Scenario

Vehicle Price: $22,000

Down Payment: $2,000

Loan Amount: $20,000

Term: 72 Months

Estimated Rate: 11.99%

Monthly Payment: Approximately $390

Total Interest: Approximately $8,080

These examples illustrate how financing costs vary according to borrower and market characteristics.

Practical Canadian Case Studies

Case Study 1: Major Financial Institution

A large Canadian lender originates thousands of vehicle loans annually. Through securitization, it converts portions of its loan portfolio into marketable securities. Capital generated from investors supports additional lending activity throughout Canada.

The result is improved liquidity, diversified funding sources, and greater lending capacity.

Case Study 2: Captive Auto Finance Company

A vehicle manufacturer’s financing division utilizes securitization to support dealership financing programs. Investors purchase securities backed by customer auto loans, enabling the company to continue offering competitive financing promotions.

This structure helps maintain vehicle sales momentum and financing availability.

Case Study 3: Alternative Lending Provider

A specialized lender serving non-prime borrowers develops securitization programs that attract institutional investors seeking diversified exposure to automotive credit assets.

The additional capital helps expand financing opportunities for consumers who may not qualify through traditional channels.

Banks vs Lenders vs Brokers Comparison

| Feature | Banks | Alternative Lenders | Brokers |

|---|---|---|---|

| Funding Sources | Deposits and capital markets | Securitization and investors | Multiple lending partners |

| Loan Options | Moderate | Broad | Extensive |

| Approval Flexibility | Lower | Higher | Varies |

| Credit Requirements | Stricter | More flexible | Multiple solutions |

| Funding Speed | Moderate | Fast | Depends on lender |

| Vehicle Types | Standard | Wider range | Multiple options |

Understanding these differences helps borrowers identify financing solutions aligned with their needs.

Future Outlook for the Canadian Auto Securitization Market

The future of Canadian auto loan ABS trends Canada continues to evolve as technology, consumer preferences, and financial markets change.

Several developments are expected to influence growth:

Digital Lending Expansion

Online applications and automated underwriting systems are increasing efficiency across the lending ecosystem.

Electric Vehicle Financing Growth

The rise of electric vehicles may create new categories within securitized automotive assets.

Enhanced Data Analytics

Advanced risk assessment technologies improve portfolio evaluation and investor confidence.

Regulatory Oversight

Continued regulatory monitoring helps maintain transparency and market stability.

Institutional Demand

Growing interest from large investors may support further development of Canadian automotive asset-backed securities markets.

Expert Approval Acceleration Tips

Consumers seeking vehicle financing can strengthen their approval prospects by following several proven strategies.

Improve Credit Health

Review credit reports regularly and address inaccuracies before applying.

Maintain Stable Employment

Consistent income helps demonstrate repayment capacity.

Reduce Existing Debt

Lower debt obligations can improve debt-service ratios.

Save for a Down Payment

Larger down payments reduce lender risk and may improve financing terms.

Organize Documentation

Prepare:

- Proof of income

- Employment verification

- Identification

- Residence information

Choose Affordable Vehicle Pricing

Selecting a vehicle within your budget improves approval potential and long-term financial sustainability.

Critical Mistakes to Avoid

Many borrowers unintentionally weaken their financing opportunities.

Applying With Multiple Lenders Simultaneously

Numerous applications within a short period can create unnecessary complications.

Ignoring Total Loan Cost

Focus on overall borrowing costs rather than monthly payments alone.

Skipping Credit Review

Understanding your credit profile before applying allows better preparation.

Choosing Excessively Long Terms

Long loan terms may increase total interest expenses.

Overestimating Affordability

Vehicle ownership includes maintenance, insurance, fuel, and registration expenses.

Incomplete Documentation

Missing paperwork can delay approvals and funding.

Frequently Asked Questions

What is auto loan securitization in Canada?

Auto loan securitization is the process of bundling vehicle loans and converting them into investment securities that are sold to institutional investors. The resulting capital allows lenders to continue financing additional vehicle purchases.

How do asset-backed car loans support securitization?

Asset-backed car loans generate predictable monthly payment streams. These payments become the underlying assets supporting securities purchased by investors, creating a funding source for lenders.

Does securitization affect my auto loan payments?

No. Borrowers generally continue making payments according to their original loan agreements. The securitization process occurs behind the scenes and usually does not alter repayment obligations.

Who invests in Canadian auto loan asset-backed securities?

Investors commonly include pension funds, insurance companies, investment managers, banks, and other institutions seeking diversified income-producing investments.

Are securitized auto loans riskier for borrowers?

The securitization structure primarily affects lenders and investors rather than borrowers. Loan terms, repayment obligations, and consumer protections remain governed by the original financing agreement.

Why do lenders use securitization?

Securitization provides immediate capital, improves liquidity, supports risk management, and enables lenders to originate additional vehicle loans without waiting years for repayment.

How do investors evaluate securitized auto finance products?

Investors analyze loan quality, borrower credit characteristics, delinquency rates, vehicle collateral values, servicing performance, and economic conditions before investing.

What is the future of auto loan securitization in Canada?

The market is expected to continue evolving through digital lending innovations, advanced analytics, growing institutional participation, and increasing demand for vehicle financing across traditional and emerging vehicle categories.

Conclusion

Auto loan securitization Canada remains a critical pillar of the Canadian automotive finance industry. By transforming vehicle loans into investment-grade securities, lenders gain access to capital that supports continued financing availability across the country. The system creates benefits for consumers, lenders, and investors while enhancing liquidity throughout the financial ecosystem.

As asset backed car loans Canada, securitized auto finance Canada, institutional investment car loans Canada, and Canadian auto loan ABS trends Canada continue developing, borrowers can expect ongoing innovation, expanded financing opportunities, and improved access to vehicle ownership solutions.

For Canadians seeking vehicle financing, understanding how the market operates behind the scenes provides valuable insight into lender funding strategies, financing availability, and long-term industry stability. Whether purchasing a first vehicle, upgrading transportation, or exploring financing alternatives, informed decisions remain the foundation of successful borrowing.

Internal Links for QuickApprovals.ca

- https://quickapprovals.ca/how-auto-financing-companies-fund-car-loans-canada/

- https://quickapprovals.ca/vehicle-loan-underwriting-process-canada/

- https://quickapprovals.ca/car-loan-risk-assessment-guide-canada/

- https://quickapprovals.ca/how-lenders-evaluate-auto-loan-applications/

- https://quickapprovals.ca/canadian-vehicle-financing-market-trends/

- https://quickapprovals.ca/alternative-auto-finance-solutions-canada/