When exploring financing options in Canada, understanding the difference between a car loan and a personal loan in Canada is crucial for making informed financial decisions. Both loan types serve distinct purposes, with unique features, benefits, and considerations that can impact your borrowing experience. Whether you’re purchasing a vehicle or funding another expense, choosing the right loan can save you money and align with your financial goals. This article provides a comprehensive comparison of these loans, leveraging insights from authoritative sources like government and bank websites. For tailored financing solutions, visit Quick Approvals.

Car Loan vs Personal Loan for Buying Car Canada: Key Overview

difference between a car loan and a personal loan in Canada, Car Loan vs Personal Loan for Buying Car Canada, Car loans and personal loans are two common financing options in Canada, each designed for specific needs. A car loan is typically a secured loan, meaning the vehicle you purchase serves as collateral, reducing the lender’s risk. In contrast, a personal loan is often unsecured, relying on your creditworthiness without requiring collateral. This fundamental difference affects interest rates car loan versus personal loan Canada, repayment terms, and overall costs. Below, we delve into the specifics to help you decide which option suits your needs.

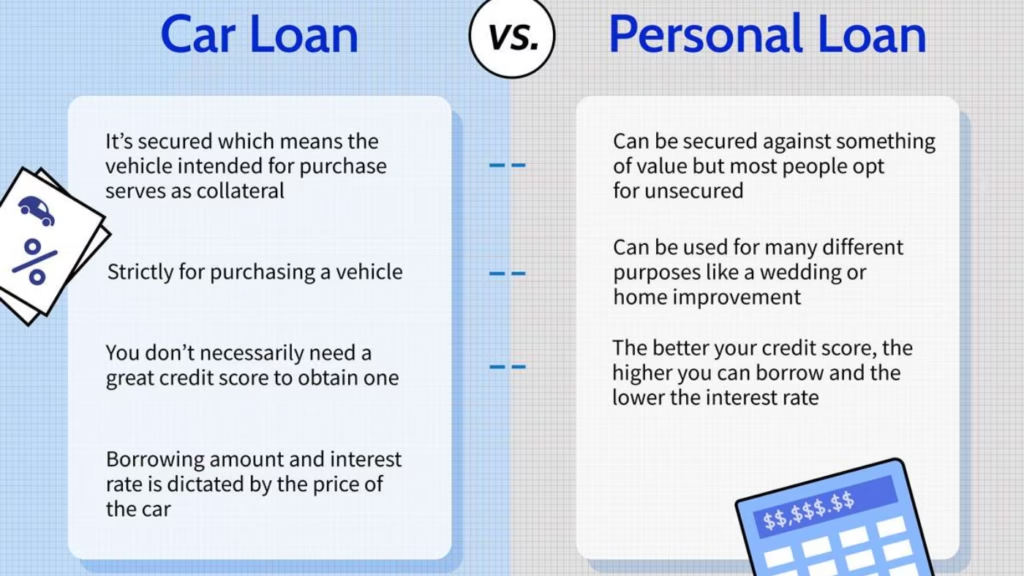

Secured vs. Unsecured Loans

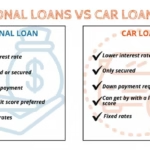

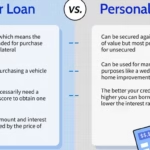

- Car Loans: These are secured loans, meaning the vehicle acts as collateral. If you default, the lender can repossess the car to recover their funds. This security often leads to lower interest rates car loan versus personal loan Canada.

- Personal Loans: Typically unsecured, personal loans don’t require collateral, increasing the lender’s risk. As a result, they often have higher interest rates but offer flexibility for various uses, from debt consolidation to home renovations.

Loan Purpose and Flexibility

- Car Loans: Designed specifically for vehicle purchases, car loans restrict funds to buying a car. Lenders may require details about the vehicle, such as its make, model, and value.

- Personal Loans: These offer greater flexibility, allowing you to use funds for any purpose, including buying a car, funding a vacation, or covering medical expenses. This makes them ideal if you prefer not to tie your loan to a specific asset.

Pros and Cons Car Loan vs Personal Loan Canada

To choose between a car loan and a personal loan, weighing their advantages and disadvantages is essential. Below is a detailed comparison:

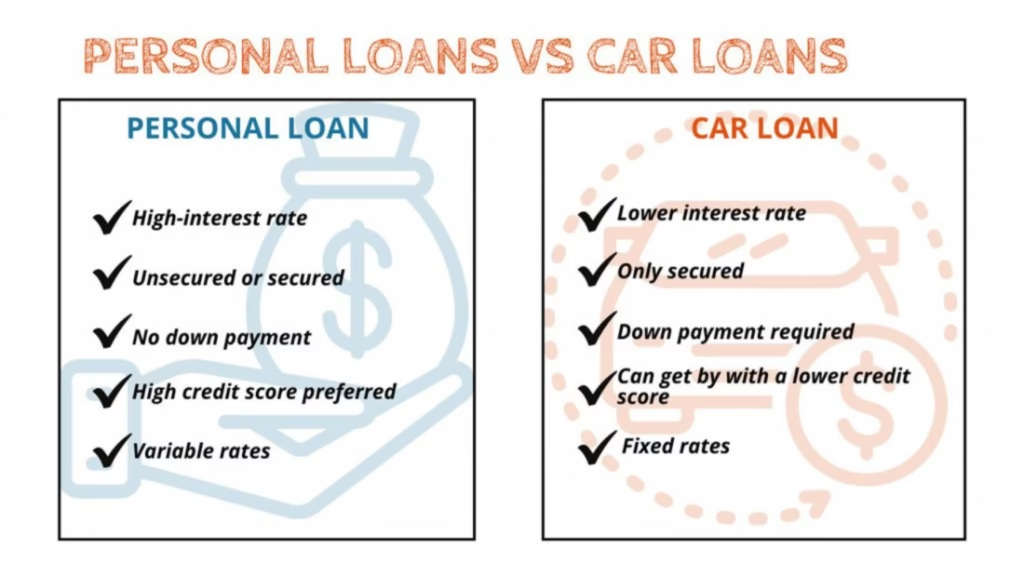

- Car Loans:

- Pros:

- Lower interest rates due to the secured nature (typically 4-7% in Canada, depending on credit).

- Fixed repayment terms aligned with the vehicle’s value.

- Potential for manufacturer or dealer incentives, such as 0% financing during promotions.

- Cons:

- Restricted to vehicle purchases, limiting flexibility.

- Risk of repossession if payments are missed.

- May require a down payment (often 10-20% of the vehicle’s value).

- Pros:

- Personal Loans:

- Pros:

- Flexible use of funds for any purpose.

- No collateral required, reducing the risk of asset loss.

- Faster approval processes for smaller amounts, especially with online lenders like Quick Approvals.

- Cons:

- Higher interest rates (often 8-15% or more, depending on credit).

- Stricter credit requirements for favorable terms.

- Potentially shorter repayment periods, increasing monthly payments.

- Pros:

Interest Rates Car Loan Versus Personal Loan Canada

Interest rates are a critical factor when comparing car loan vs personal loan for buying car Canada. According to the Bank of Canada, recent rate hikes have influenced borrowing costs, with car loans generally offering lower rates due to their secured nature. For example:

- Car Loans: Rates typically range from 4-7% for borrowers with good credit, as the vehicle collateral reduces lender risk.

- Personal Loans: Rates often range from 8-15% or higher, especially for unsecured loans, as lenders rely solely on your credit score and income.

To secure the best rates, compare offers from multiple lenders, including banks, credit unions, and online platforms like Quick Approvals.

Repayment Terms Car Loan Personal Loan Canada

Repayment terms significantly impact your monthly budget and total loan cost. Here’s how they differ:

- Car Loans: Terms typically range from 36 to 84 months, aligned with the vehicle’s depreciation. Longer terms reduce monthly payments but increase total interest paid.

- Personal Loans: Terms are often shorter, ranging from 12 to 60 months. Shorter terms mean higher monthly payments but lower overall interest costs.

Repayment Terms Car Loan Personal Loan Canada, For example, a $20,000 car loan at 5% over 60 months results in monthly payments of approximately $377, with total interest of about $2,620. A $20,000 personal loan at 10% over 36 months has monthly payments of about $664, with total interest of around $3,904. Use loan calculators from trusted sources like RBC Royal Bank to estimate your payments.

Secured Car Loan vs Unsecured Personal Loan Canada

The distinction between secured car loan vs unsecured personal loan Canada affects risk, cost, and eligibility:

- Secured Car Loans: The vehicle secures the loan, lowering interest rates and making approval easier, even for those with moderate credit. However, defaulting risks repossession.

- Unsecured Personal Loans: These rely on your credit score and income, making approval harder for those with poor credit. They offer flexibility but come with higher rates and stricter eligibility criteria.

Applying for Car Loan vs Personal Loan Canada

The application process for both loans varies:

- Car Loans: Often processed through dealerships or lenders, requiring vehicle details, proof of income, and credit checks. Dealerships may streamline applications but could include higher rates or fees.

- Personal Loans: Available through banks, credit unions, or online lenders, requiring proof of income, credit history, and sometimes employment verification. Online platforms like Quick Approvals offer quick pre-approval processes.

Tax Benefits Car Loan vs Personal Loan Canada

Tax implications can influence your decision:

- Car Loans: Interest on car loans is generally not tax-deductible for personal use. However, if the vehicle is used for business purposes (e.g., delivery services), you may claim deductions on interest and depreciation, subject to Canada Revenue Agency (CRA) rules.

- Personal Loans: Interest is typically not deductible unless the loan is used for income-generating purposes, such as investing in a business.

Consult a tax professional or review CRA guidelines for specific deductions.

Q&A: Common Questions About Car Loan vs Personal Loan for Buying Car Canada

Which Is Better Car Loan or Personal Loan Canada?

The choice depends on your needs. A car loan vs personal loan for buying car Canada comparison shows car loans offer lower rates (4-7%) due to collateral, ideal for vehicle purchases. Personal loans provide flexibility for other expenses but come with higher rates (8-15%). If your priority is cost, a car loan is better; for flexibility, choose a personal loan.

How to Choose Car Loan or Personal Loan Canada?

Consider your purpose, budget, and credit. For vehicle purchases, a car loan vs personal loan for buying car Canada offers lower rates and longer terms. If you need funds for multiple purposes or lack collateral, a personal loan is better. Compare offers from lenders like Quick Approvals to find the best terms.

What Is the Difference Between a Car Loan and a Personal Loan in Canada?

The difference between a car loan and a personal loan in Canada lies in security, purpose, and cost. Car loans are secured, with lower rates (4-7%) and restricted to vehicles. Personal loans are unsecured, with higher rates (8-15%) and flexible use. Car loans risk repossession, while personal loans rely on creditworthiness.

Is a Personal Loan Better Than a Car Loan in Canada?

It depends on your goals. A personal loan better than a car loan in Canada if you value flexibility or want to avoid collateral. However, car loans are cheaper for vehicle purchases due to lower rates. Assess your financial situation and compare rates from trusted sources like the Bank of Canada.

What Are the Repayment Terms for Car Loan vs Personal Loan Canada?

Repayment terms car loan personal loan Canada vary. Car loans offer 36-84 months, with lower monthly payments but higher total interest. Personal loans range from 12-60 months, with higher payments but lower overall interest. Use loan calculators to evaluate affordability.

Conclusion

Understanding the difference between a car loan and a personal loan in Canada empowers you to make informed financial choices. Car loans offer lower interest rates car loan versus personal loan Canada and are ideal for vehicle purchases, while personal loans provide flexibility for various needs. By considering pros and cons car loan vs personal loan Canada, repayment terms, and tax implications, you can select the best option for your budget. For personalized financing solutions, explore Quick Approvals. For further insights, consult authoritative resources like the Bank of Canada or RBC Royal Bank to stay informed about rates and terms.