Buying a vehicle is one of the largest financial commitments many Canadians make outside of purchasing a home. While shoppers often spend significant time comparing vehicle models, dealerships, and features, many overlook one of the most important financial decisions in the process: choosing the right loan structure.

The debate surrounding variable vs fixed car loans Canada continues to grow as interest rates fluctuate and economic conditions evolve. The loan type you choose can influence your monthly payments, total borrowing costs, budgeting flexibility, and overall financial stability throughout the loan term.

For some borrowers, predictable payments offer peace of mind and easier financial planning. For others, a flexible rate structure may create opportunities for savings when market rates decline. Understanding the differences is essential before signing any financing agreement.

This guide explains how variable and fixed auto loans work in Canada, compares their advantages and disadvantages, outlines eligibility requirements, examines cost implications, and provides practical examples to help you make an informed borrowing decision. variable vs fixed car loans Canada

Understanding Variable vs Fixed Car Loans Canada

A car loan allows borrowers to spread vehicle purchase costs over a predetermined period while paying interest to the lender. The primary distinction between loan structures lies in how interest rates are calculated throughout the repayment period. variable vs fixed car loans Canada

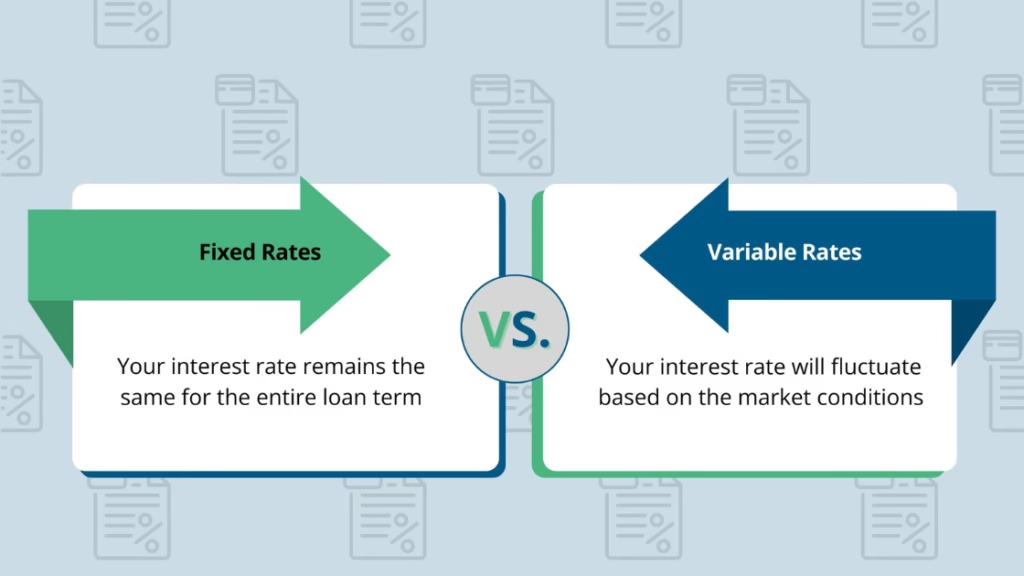

Fixed Rate Auto Loans

A fixed-rate loan maintains the same interest rate throughout the entire term. Monthly payments remain unchanged regardless of market interest rate movements. variable vs fixed car loans Canada

Benefits include:

- Predictable monthly payments

- Easier budgeting

- Protection against rising interest rates

- Consistent repayment schedule

Potential drawbacks include:

- Less opportunity to benefit from falling rates

- Sometimes slightly higher initial rates

- Reduced flexibility depending on lender policies

Variable Rate Auto Loans

Variable-rate auto loans have interest rates that can change based on broader market conditions and benchmark lending rates.

Benefits include:

- Potential savings if rates decline

- Lower starting rates in some market environments

- Greater flexibility in certain lending programs

Potential drawbacks include:

- Payment uncertainty

- Increased financial risk

- Higher costs if interest rates rise

Understanding these fundamental differences is the first step toward making the right borrowing decision. variable vs fixed car loans Canada

How Choose Variable or Fixed Auto Loan Canada Decisions Affect Your Finances

Selecting between fixed and variable financing impacts more than your monthly payment. It affects long-term affordability, financial planning, and risk exposure. Choose Variable or Fixed Auto Loan Canada

When borrowers choose variable or fixed auto loan Canada financing, they should evaluate:

Income Stability

Borrowers with predictable salaries often have greater flexibility when considering variable-rate financing.

Individuals with seasonal, commission-based, or inconsistent income may prefer fixed payments for budgeting certainty. Choose Variable or Fixed Auto Loan Canada

Risk Tolerance

Every borrower has a different comfort level with financial uncertainty.

If rising payments would create stress or financial strain, fixed financing may be the better choice.

Loan Duration

Longer loan terms increase exposure to future interest-rate changes.

Variable-rate loans become more sensitive to economic shifts over five to eight years than shorter financing periods.

Economic Outlook

Market forecasts can influence borrowing strategies, though no one can predict future interest-rate movements with certainty.

The safest decision is usually based on personal financial circumstances rather than speculation. Choose Variable or Fixed Auto Loan Canada

The Canadian Auto Financing Landscape

Canadian borrowers typically obtain vehicle financing through:

- Banks

- Credit unions

- Alternative lenders

- Dealership financing departments

- Auto loan brokers

Each lender evaluates:

- Credit history

- Debt levels

- Employment stability

- Income verification

- Vehicle characteristics

While fixed-rate financing remains the most common auto loan structure in Canada, some lenders and financing partners offer variable-rate options for qualified borrowers.

Understanding lender preferences helps borrowers compare available financing opportunities more effectively.

Step-by-Step Guide to Comparing Loan Structures

Step 1: Assess Your Monthly Budget

The first priority should be determining how much you can comfortably afford each month.

Vehicle ownership includes:

- Loan payments

- Insurance

- Maintenance

- Fuel or charging costs

- Registration fees

Avoid stretching your budget based solely on lender approval amounts.

Step 2: Analyze Current Variable Fixed Rates Canada

Interest rates play a major role in financing decisions.

When evaluating current variable fixed rates Canada, borrowers should compare:

| Comparison Factor | Fixed Rate Loan | Variable Rate Loan |

|---|---|---|

| Rate Stability | Constant | Changes Over Time |

| Monthly Payment Predictability | High | Moderate to Low |

| Exposure to Rate Increases | None | Yes |

| Potential Benefit from Rate Cuts | No | Yes |

| Budgeting Simplicity | Excellent | Moderate |

Rate comparisons should always include: current variable fixed rates Canada

- Annual Percentage Rate (APR)

- Loan term

- Fees

- Optional products

- Total repayment cost

The lowest advertised rate is not always the lowest-cost financing option. current variable fixed rates Canada

Step 3: Review Total Loan Costs

Many borrowers focus only on monthly payments.

A better approach is calculating:

- Total interest paid

- Total repayment amount

- Potential future payment changes

- Early repayment opportunities

This provides a clearer picture of actual borrowing costs.

Step 4: Evaluate Future Financial Plans

Consider upcoming life events such as:

- Home purchases

- Family expansion

- Career changes

- Education expenses

Stable payments may become more valuable if major financial commitments are expected during the loan term.

Step 5: Compare Multiple Lenders

Never accept the first financing offer.

Request quotes from:

- Banks

- Credit unions

- Online lenders

- Auto finance specialists

- Loan brokers

Multiple comparisons often reveal significant cost differences.

Eligibility Requirements for Canadian Auto Loans

Regardless of rate structure, most lenders require borrowers to meet specific qualifications.

Basic Requirements

Applicants typically need:

- Canadian residency

- Age of majority in their province

- Valid identification

- Verifiable income

- Active bank account

Employment Requirements

Lenders generally prefer:

- Full-time employment

- Stable income history

- Consistent earnings

Self-employed applicants may need additional documentation.

Credit Requirements

Approval standards vary widely.

Borrowers may qualify with:

- Excellent credit

- Good credit

- Fair credit

- Challenged credit

- Previous credit difficulties

Higher credit scores generally provide access to more competitive financing options.

Understanding Risk Comparison Car Loans Canada

One of the most important factors when evaluating financing options is risk. Risk Comparison Car Loans Canada

The risk comparison car loans Canada analysis should focus on how changing interest rates could affect affordability over time.

Fixed Loan Risk Profile

Fixed-rate loans offer: Risk Comparison Car Loans Canada

- Predictable expenses

- Consistent payment schedules

- Protection from market volatility

Primary risk:

- Missing potential savings during declining-rate environments

Variable Loan Risk Profile

Variable-rate loans offer:

- Potential cost reductions

- Greater sensitivity to market conditions

Primary risks:

- Payment increases

- Higher long-term interest costs

- Budget uncertainty

Borrowers who prioritize stability often favor fixed rates, while those comfortable managing rate fluctuations may consider variable financing. Risk Comparison Car Loans Canada

Interest Rates and Cost Breakdown

The following example illustrates how financing costs may differ.

Example Vehicle Purchase

Vehicle Price: $35,000

Down Payment: $5,000

Loan Amount: $30,000

Loan Term: 72 Months

| Scenario | Starting Rate | Monthly Payment | Total Interest Paid |

|---|---|---|---|

| Fixed Rate Loan | 6.99% | Approximately $512 | Approximately $6,864 |

| Variable Rate Loan (Rate Unchanged) | 6.49% | Approximately $502 | Approximately $6,144 |

| Variable Rate Loan (Rate Increases) | 8.49% Average | Higher Over Time | Significantly Higher |

Actual lender terms vary, but the example highlights how future rate movements can influence total borrowing costs.

Can You Switch Loan Types Canada After Financing?

Many borrowers wonder whether they can switch loan types Canada after securing financing.

The answer depends on lender policies.

Potential options include:

Refinancing

Refinancing replaces an existing loan with a new one.

Reasons include:

- Lower interest rates

- Improved credit profile

- Different loan structure

- Reduced monthly payments

Loan Restructuring

Some lenders may allow modifications without full refinancing.

Availability varies significantly.

Trade-In Financing

Borrowers replacing vehicles may effectively move into a different loan structure during a new purchase transaction.

Always review penalties, fees, and refinancing costs before making changes. Switch Loan Types Canada

Canadian Borrower Case Studies

Case Study 1: First-Time Buyer

Sarah purchased her first vehicle after securing stable full-time employment.

Priorities:

- Budget certainty

- Predictable expenses

- Long-term planning

Solution:

A fixed-rate loan aligned with her financial goals and eliminated concerns about future payment increases.

Case Study 2: High-Income Professional

Michael had strong income growth prospects and substantial savings.

Priorities:

- Lower initial borrowing costs

- Financial flexibility

- Ability to absorb payment fluctuations

Solution:

A variable-rate structure matched his higher risk tolerance.

Case Study 3: Family Budget Focus

A growing family needed a reliable SUV while managing childcare expenses and mortgage payments.

Priorities:

- Stable household budgeting

- Protection from rising rates

- Long-term affordability

Solution:

Fixed-rate financing provided greater confidence and predictable cash flow management.

Comparing Banks, Lenders, and Brokers

| Feature | Banks | Alternative Lenders | Auto Loan Brokers |

|---|---|---|---|

| Product Variety | Moderate | High | Very High |

| Credit Flexibility | Moderate | High | High |

| Approval Speed | Moderate | Fast | Fast |

| Rate Shopping | Limited | Limited | Extensive |

| Multiple Lender Access | No | No | Yes |

| Borrower Convenience | Good | Good | Excellent |

Brokers can help borrowers compare multiple financing sources simultaneously, potentially improving approval opportunities and rate competitiveness.

Expert Tips for Faster Approval

Maintain Consistent Employment

Stable employment improves lender confidence and underwriting outcomes.

Reduce Existing Debt

Lower debt obligations strengthen affordability calculations.

Improve Credit Before Applying

Even small credit score improvements may enhance financing options.

Save for a Larger Down Payment

Higher down payments can reduce borrowing costs and improve approval odds.

Verify Income Documentation

Providing complete and accurate documentation helps accelerate approval processing.

Review Credit Reports

Correcting reporting errors before applying can improve financing opportunities.

Common Mistakes to Avoid

Choosing Based Only on Monthly Payments

Low payments can conceal higher overall borrowing costs.

Ignoring Total Interest Costs

Always compare complete repayment amounts.

Failing to Compare Multiple Offers

One lender rarely represents the entire market.

Underestimating Variable Rate Risk

Future rate increases can significantly affect affordability.

Financing Beyond Vehicle Ownership Plans

Long loan terms may outlast intended vehicle ownership.

Overlooking Refinancing Opportunities

Improved credit profiles can create future savings opportunities.

Frequently Asked Questions

Is a fixed car loan better than a variable car loan in Canada?

Neither option is universally better. Fixed loans provide payment stability and protection from interest-rate increases. Variable loans may offer savings when rates decline. The best choice depends on financial goals, risk tolerance, and budgeting preferences.

How do lenders determine variable auto loan rates?

Variable rates are generally influenced by benchmark lending rates, market conditions, lender policies, borrower credit profiles, and overall economic trends. Changes in these factors can affect future borrowing costs.

Are fixed auto loan rates usually higher?

Fixed rates can sometimes start slightly higher because lenders assume the risk of future interest-rate increases. However, the difference varies based on market conditions and lender pricing strategies.

Can bad-credit borrowers obtain fixed-rate financing?

Yes. Many lenders offer fixed-rate financing to borrowers with challenged credit histories. Interest rates may be higher, but approval remains possible depending on income and overall financial circumstances.

What happens if rates rise on a variable loan?

Borrowers may experience higher monthly payments, increased interest costs, or extended repayment periods depending on loan structure and lender terms.

Is refinancing worth considering?

Refinancing can be beneficial if credit scores improve, market rates decline, or borrowers want a different loan structure. Cost-benefit analysis is important before proceeding.

How long are most Canadian car loans?

Common loan terms range from 36 to 84 months. Some lenders may offer longer financing periods depending on vehicle value and borrower qualifications.

Which loan type is best for budgeting?

Fixed-rate financing generally provides the greatest budgeting certainty because payments remain consistent throughout the loan term.

Conclusion

Choosing between variable vs fixed car loans Canada financing requires balancing cost, flexibility, and financial security. Fixed-rate loans offer predictability and protection from rising interest rates, making them ideal for borrowers who prioritize stability. Variable-rate loans can create savings opportunities when rates decline, but they also introduce uncertainty and additional financial risk.

Before making a decision, carefully evaluate your income stability, financial goals, risk tolerance, and long-term budgeting needs. Compare multiple lenders, review total repayment costs, and ensure the financing structure aligns with your overall financial strategy.

For borrowers seeking competitive vehicle financing solutions across Canada, working with experienced lending professionals can simplify the process, expand lender access, and help identify financing options tailored to individual circumstances.

Internal Links for quickapprovals.ca

- https://quickapprovals.ca/fixed-rate-auto-financing-canada-guide/

- https://quickapprovals.ca/car-loan-refinancing-options-canada/

- https://quickapprovals.ca/how-auto-loan-brokers-help-canadian-borrowers/

- https://quickapprovals.ca/understanding-car-loan-interest-costs-canada/

- https://quickapprovals.ca/best-vehicle-financing-strategies-for-first-time-buyers/

- https://quickapprovals.ca/improve-car-loan-approval-chances-canada/