Understanding 72 Month Car Loans Canada

Buying a vehicle in Canada has become significantly more expensive over the past few years. Rising vehicle prices, higher interest rates, insurance costs, and inflation have pushed many buyers toward longer financing terms to make monthly payments manageable. That is why 72 month car loans Canada have become one of the most common financing choices for both new and used vehicle buyers.

A 72-month auto loan spreads vehicle payments across six years, helping Canadians reduce monthly financial pressure while still qualifying for newer and more reliable vehicles. For many borrowers, especially first-time buyers, self-employed individuals, growing families, and buyers rebuilding credit, this financing structure creates flexibility that shorter loan terms may not provide.

However, while lower monthly payments can make ownership easier, longer financing periods also increase the total interest paid over time. Understanding how these loans work, when they make sense, and how to secure the best approval terms is critical before signing any agreement.

This complete guide explains everything Canadians need to know about 6 year auto financing Canada, including eligibility requirements, lender comparisons, approval strategies, interest rates, practical examples, and expert financial insights to help borrowers make smarter vehicle financing decisions. 72 month car loans Canada

What Is a 72 Month Car Loan?

A medium term car loans Canada arrangement allows borrowers to finance a vehicle over a period of 72 months, or six years. Instead of paying a high monthly amount over a shorter period like 36 or 48 months, borrowers spread payments over a longer duration. 72 month car loans Canada

This financing structure is commonly offered by: medium term car loans Canada

- Banks

- Credit unions

- Dealership finance departments

- Online lenders

- Auto financing brokers

The biggest reason Canadians choose this structure is affordability. Longer terms reduce monthly payments, which can help borrowers qualify for more reliable vehicles without overwhelming their monthly budgets.

For example:

| Loan Amount | Interest Rate | Loan Term | Approx Monthly Payment |

|---|---|---|---|

| $25,000 | 6.99% | 48 Months | $598 |

| $25,000 | 6.99% | 60 Months | $495 |

| $25,000 | 6.99% | 72 Months | $423 |

While the 72-month term lowers payments significantly, the borrower pays more interest overall because the loan remains active longer.

This financing option is especially common for:

- SUVs and trucks

- Electric vehicles

- Family vehicles

- New vehicle purchases

- Higher-priced used vehicles

As vehicle prices continue climbing across Canada, lenders increasingly structure approvals around affordability instead of shorter repayment speed.

Why Canadians Choose 6 Year Auto Financing

The popularity of 6 year auto financing Canada continues growing because it solves several financial challenges modern borrowers face. Many Canadians prioritize manageable monthly expenses over aggressive repayment schedules.

One major factor is vehicle affordability. Average new vehicle prices in Canada now regularly exceed $45,000. Even reliable used vehicles can cost $20,000 to $35,000. Without extended financing, monthly payments may become unrealistic for average-income households. 6 year auto financing Canada

Another reason is budgeting flexibility. A longer term helps borrowers balance: 6 year auto financing Canada

- Mortgage or rent payments

- Insurance costs

- Childcare expenses

- Grocery inflation

- Existing debt obligations

Many borrowers also prefer keeping emergency savings available rather than making large down payments. Extended financing allows them to preserve liquidity while still purchasing dependable transportation.

Modern lenders additionally recognize that newer vehicles often remain reliable longer than older models. Because of improved manufacturing standards, financing a vehicle over six years is now more common than it was a decade ago.

Borrowers rebuilding credit may also benefit from extended terms because lower payments reduce debt-to-income strain and improve approval chances.

Still, choosing this loan structure should always involve careful analysis of long-term ownership goals and total financing costs.

How 72 Month Auto Financing Works in Canada

Understanding the mechanics of 72 month loan rates Canada helps borrowers make informed decisions before accepting financing offers.

When you apply for vehicle financing, lenders evaluate several financial factors:

- Credit score

- Income stability

- Employment history

- Existing debt

- Vehicle age and mileage

- Down payment amount

Once approved, the lender provides a fixed loan amount that includes:

- Vehicle purchase price

- Taxes

- Dealer fees

- Warranty products (if included)

- Registration fees

The borrower then repays the balance through scheduled monthly, bi-weekly, or weekly payments over 72 months.

Most Canadian vehicle loans use fixed interest rates, meaning payments remain stable throughout the financing term.

Key loan components include:

Principal Balance

The amount borrowed after the down payment.

Interest Charges

The lender’s cost for financing the loan.

Amortization Schedule

The repayment timeline showing how payments apply toward principal and interest.

Residual Vehicle Value

The expected value of the vehicle during and after the loan term.

Longer financing terms reduce monthly costs but slow principal reduction during the early years of the loan.

Pros and Cons of 72 Month Car Loans Canada

Understanding 72 months pros cons Canada is essential before selecting a longer financing structure.

Advantages of 72-Month Financing

Lower Monthly Payments

The biggest advantage is affordability. Lower payments help buyers qualify for vehicles without overwhelming their monthly cash flow. 72 months pros cons Canada

Access to Better Vehicles

Borrowers may afford newer, safer, and more fuel-efficient vehicles that would otherwise exceed budget limitations.

Easier Approval Qualification

Lower monthly obligations improve debt ratios, helping some applicants qualify more easily.

Financial Flexibility

Borrowers can preserve savings for emergencies, investments, or home expenses instead of making large upfront vehicle payments.

Predictable Budgeting

Fixed-rate financing creates stable monthly transportation costs. 72 months pros cons Canada

Disadvantages of 72-Month Financing

Higher Total Interest

Longer loans accumulate more interest over time.

Negative Equity Risk

Borrowers may owe more than the vehicle’s value during early years of the loan.

Longer Financial Commitment

Six years is a significant repayment period that may outlast ownership goals.

Increased Insurance Costs

Lenders often require comprehensive insurance coverage throughout the loan term.

Slower Vehicle Equity Growth

Long-term loans reduce how quickly borrowers build ownership value.

The best financing decision depends on balancing affordability with long-term financial efficiency.

Eligibility Requirements for 72 Month Car Loans Canada

Qualifying for medium term car loans Canada depends on both borrower strength and vehicle eligibility.

Most lenders require:

| Requirement | Typical Expectation |

|---|---|

| Minimum Age | 18 or 19 depending on province |

| Residency | Canadian resident |

| Income Stability | Consistent employment or income |

| Credit Score | Usually 600+ preferred |

| Valid Identification | Government-issued ID |

| Bank Account | Active Canadian account |

| Insurance | Full vehicle coverage |

| Vehicle Criteria | Approved age and mileage limits |

Applicants with strong credit usually access better rates and more flexible terms.

However, alternative lenders and brokers may still approve borrowers with:

- Bad credit

- Previous bankruptcy

- Consumer proposal history

- Limited credit history

- Self-employment income

Income verification may include:

- Pay stubs

- Tax returns

- Bank statements

- T4 slips

- Employer confirmation

The stronger the financial profile, the lower the financing risk for lenders.

Typical 72 Month Loan Rates Canada

Current 72 month loan rates Canada vary depending on several factors, including market interest rates, borrower credit strength, and vehicle type.

Average Rate Ranges

| Borrower Type | Estimated Rate Range |

|---|---|

| Excellent Credit | 4.99% – 6.99% |

| Good Credit | 6.99% – 9.99% |

| Fair Credit | 9.99% – 14.99% |

| Bad Credit | 15.99% – 24.99% |

Several variables affect rates:

- Bank of Canada rate environment

- Vehicle age

- Down payment amount

- Debt-to-income ratio

- Lender risk tolerance

- Loan amount

New vehicles generally receive lower rates than used vehicles because they retain value better.

Borrowers can often reduce interest costs by:

- Improving credit scores

- Increasing down payments

- Reducing existing debt

- Choosing newer vehicles

- Adding co-signers

Rate shopping through multiple lenders or brokers can significantly improve final financing terms.

Real Canadian Cost Examples for 72 Month Financing

Understanding actual borrowing costs helps Canadians evaluate whether extended financing fits their financial goals.

Example 1: New SUV Financing

| Details | Amount |

|---|---|

| Vehicle Price | $42,000 |

| Down Payment | $4,000 |

| Loan Amount | $38,000 |

| Interest Rate | 6.49% |

| Loan Term | 72 Months |

| Monthly Payment | Approx. $640 |

| Total Interest Paid | Approx. $8,080 |

Example 2: Used Sedan Financing

| Details | Amount |

|---|---|

| Vehicle Price | $24,000 |

| Down Payment | $2,000 |

| Loan Amount | $22,000 |

| Interest Rate | 9.99% |

| Loan Term | 72 Months |

| Monthly Payment | Approx. $405 |

| Total Interest Paid | Approx. $7,160 |

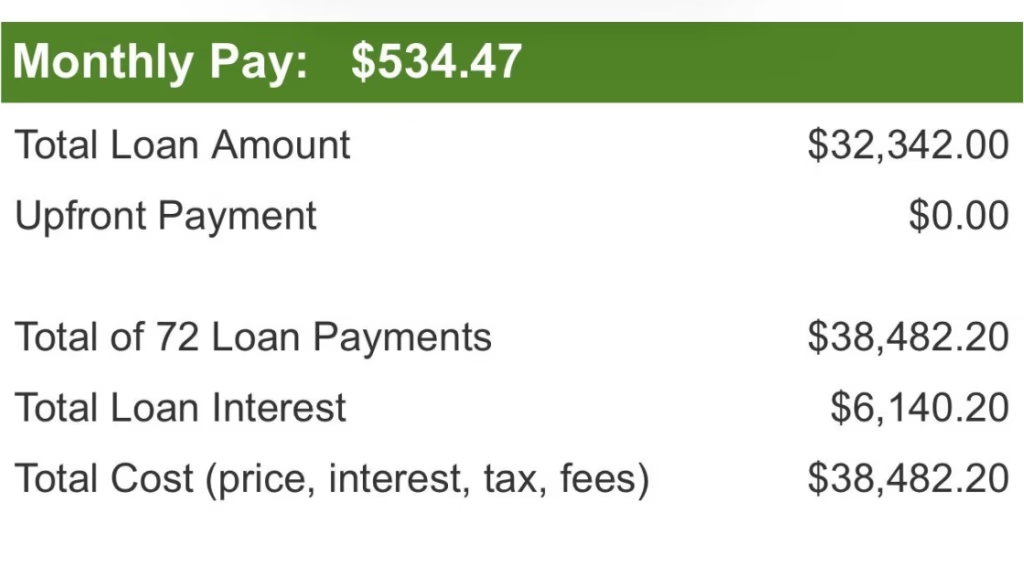

Example 3: Bad Credit Truck Financing

| Details | Amount |

|---|---|

| Vehicle Price | $32,000 |

| Down Payment | $1,500 |

| Loan Amount | $30,500 |

| Interest Rate | 18.99% |

| Loan Term | 72 Months |

| Monthly Payment | Approx. $703 |

| Total Interest Paid | Approx. $20,100 |

These examples show how interest rates dramatically influence overall borrowing costs.

Banks vs Lenders vs Brokers in Canada

Choosing the right financing source is critical when seeking 6 year auto financing Canada.

| Feature | Banks | Alternative Lenders | Auto Loan Brokers |

|---|---|---|---|

| Credit Flexibility | Low | High | Very High |

| Interest Rates | Lower | Higher | Competitive |

| Approval Speed | Moderate | Fast | Very Fast |

| Bad Credit Options | Limited | Strong | Strong |

| Vehicle Restrictions | More Strict | Flexible | Flexible |

| Custom Solutions | Limited | Moderate | High |

| Income Flexibility | Moderate | Flexible | Flexible |

Banks

Banks often offer the best rates but maintain stricter approval requirements.

Best for:

- Excellent credit

- Stable employment

- Strong debt ratios

Alternative Lenders

Alternative finance companies focus on higher-risk borrowers.

Best for:

- Credit rebuilding

- Self-employed borrowers

- Limited credit history

Auto Loan Brokers

Brokers compare multiple lenders simultaneously.

Best for:

- Rate shopping

- Faster approvals

- Complicated financial situations

Many Canadians benefit from broker networks because they increase approval opportunities while reducing application stress.

Step-by-Step Guide to Getting Approved

Securing 72 month car loans Canada becomes easier when borrowers prepare strategically.

Step 1: Review Your Credit

Check credit reports for:

- Errors

- High balances

- Missed payments

- Collection accounts

Improving even small credit issues may significantly reduce financing costs.

Step 2: Calculate Your Budget

Consider:

- Fuel

- Insurance

- Maintenance

- Registration

- Winter tires

- Parking costs

Avoid financing solely based on maximum approval limits.

Step 3: Save a Down Payment

Even modest down payments improve:

- Approval odds

- Interest rates

- Monthly payments

- Equity position

Step 4: Compare Multiple Financing Sources

Never accept the first offer automatically.

Compare:

- Interest rates

- Loan terms

- Prepayment penalties

- Dealer fees

- Warranty costs

Step 5: Choose the Right Vehicle

Lenders prefer vehicles with:

- Lower mileage

- Reliable history

- Strong resale value

- Clean accident records

Step 6: Submit Complete Documentation

Missing paperwork delays approvals.

Typical requirements include:

- Driver’s licence

- Income proof

- Residence verification

- Insurance details

Expert Approval Acceleration Tips

Improving approval strength for 72 month loan rates Canada often requires strategic financial preparation.

Reduce Existing Debt

Lower debt ratios improve lender confidence and may reduce rates.

Avoid Multiple Credit Applications

Too many hard inquiries may reduce credit scores temporarily.

Consider a Co-Signer

Strong co-signers help borrowers access:

- Lower rates

- Larger approvals

- Better loan terms

Increase Employment Stability

Lenders prefer:

- Longer employment duration

- Consistent income history

- Stable industries

Finance Within Realistic Limits

Overextending financially increases rejection risk.

Borrowers should prioritize affordability rather than maximum loan amounts.

Common Mistakes Canadians Should Avoid

Many borrowers make financing decisions based only on monthly payment size. This can create long-term financial problems.

Ignoring Total Interest Costs

Low payments may hide thousands in additional borrowing expenses.

Financing Depreciating Luxury Vehicles

Rapid depreciation increases negative equity risks.

Skipping Vehicle Inspections

Used vehicle problems may create repair costs while loan balances remain high.

Rolling Old Debt Into New Loans

Adding previous loan balances increases financial strain.

Choosing Longer Terms Without a Strategy

Extended financing should support broader financial goals, not compensate for overspending.

Canadian Case Studies

Case Study 1: First-Time Buyer in Ontario

A 28-year-old professional purchased a $29,000 sedan using medium term car loans Canada financing.

Key Results:

- 72-month loan

- 6.99% rate

- $3,000 down payment

- Monthly payment under $450

The longer term helped preserve emergency savings while establishing credit history.

Case Study 2: Self-Employed Contractor in Alberta

A contractor with fluctuating income struggled securing bank financing.

Using a broker:

- Approved through alternative lender

- 72-month truck financing

- Flexible income verification accepted

The vehicle supported business operations while maintaining manageable cash flow.

Case Study 3: Credit Rebuilding Borrower in British Columbia

After recovering from financial hardship, a borrower secured:

- Used SUV financing

- Higher interest rate initially

- Opportunity to refinance after 18 months

Responsible payment history later improved refinancing eligibility.

When a 72 Month Loan Makes Sense

A 6 year auto financing Canada strategy may work well when:

- Monthly budget flexibility matters

- Vehicle reliability is essential

- Interest rates remain competitive

- Buyers plan long-term ownership

- Emergency savings preservation is important

Longer terms are often practical for:

- Families

- Commuters

- Rural drivers

- Business vehicle users

However, borrowers should avoid excessively long financing on vehicles likely to depreciate rapidly.

How to Pay Off a 72 Month Car Loan Faster

Even if borrowers choose extended financing, they can still reduce long-term interest costs.

Make Lump-Sum Payments

Tax refunds or bonuses can reduce principal faster.

Increase Bi-Weekly Payments

Small increases shorten repayment timelines significantly.

Refinance After Credit Improvement

Improved credit may qualify borrowers for lower rates later.

Avoid Payment Deferrals

Skipped payments extend interest accumulation.

Round Up Monthly Payments

Even modest additional amounts help reduce total borrowing costs.

Frequently Asked Questions

Are 72 month car loans common in Canada?

Yes. 72 month car loans Canada are now extremely common because vehicle prices have increased substantially. Many lenders and dealerships regularly offer six-year financing terms for both new and used vehicles.

Is a 72 month car loan a good idea?

It depends on financial goals, budget flexibility, and total borrowing costs. A 72-month loan can improve affordability, but borrowers should evaluate total interest expenses carefully before committing.

What credit score is needed for 72 month financing?

Most traditional lenders prefer scores above 650. However, many alternative lenders approve borrowers with lower scores depending on income, down payment, and vehicle selection.

Can I get 72 month financing with bad credit?

Yes. Many Canadian lenders specialize in bad-credit auto financing. Interest rates may be higher, but approval remains possible with stable income and realistic vehicle choices.

Are used cars eligible for 72 month loans?

Yes, although lender restrictions may apply regarding:

Vehicle age

Mileage

Condition

Market value

Newer used vehicles typically qualify more easily.

Can I pay off a 72 month loan early?

Most Canadian auto loans allow early repayment without penalties. Borrowers should always confirm prepayment policies before signing financing agreements.

Do longer loans hurt credit scores?

Not directly. Making consistent on-time payments can actually strengthen credit history. Problems arise only if borrowers miss payments or carry excessive debt.

Should I choose 60 or 72 month financing?

The best option depends on:

Monthly budget

Interest rate

Vehicle value

Ownership plans

Long-term financial priorities

Borrowers should compare total loan costs alongside monthly payment affordability.

Final Thoughts on 72 Month Car Loans Canada

For many Canadians, 72 month car loans Canada provide a practical path toward vehicle ownership in an increasingly expensive automotive market. Lower monthly payments create flexibility, improve affordability, and help borrowers access safer and more reliable transportation.

However, extended financing should always be approached strategically. Understanding total borrowing costs, interest rates, depreciation risks, and lender requirements is essential before committing to a six-year repayment structure.

The smartest borrowers focus on balancing affordability with long-term financial efficiency. Choosing the right vehicle, improving credit health, comparing lenders carefully, and making extra payments whenever possible can significantly reduce overall financing costs.

Whether you are purchasing your first vehicle, rebuilding credit, or upgrading to a family SUV, the right financing strategy can help you secure approval confidently while protecting your long-term financial health.

To explore personalized financing solutions, compare lender options, and improve approval chances, visit Quick Approvals Canada for tailored Canadian auto loan support.

Internal Links for quickapprovals.ca

- https://quickapprovals.ca/bad-credit-auto-loans-ontario/

- https://quickapprovals.ca/how-car-loan-interest-rates-work-canada/

- https://quickapprovals.ca/used-car-financing-guide-canada/

- https://quickapprovals.ca/auto-loan-pre-approval-canada/

- https://quickapprovals.ca/car-loan-refinancing-options-canada/

- https://quickapprovals.ca/self-employed-car-loans-canada/